IRS: Employee vs. Independent Contractor—Ten IRS Tips for Business Owners

IRS Summertime Tax Tip 2009-20

If you are a small business owner, whether you hire people as independent contractors or as employees will impact how much taxes you pay and the amount of taxes you withhold from their paychecks. Additionally, it will affect how much additional cost your business must bear, what documents and information they must provide to you, and what tax documents you must give to them.

Here are the top ten things every business owner should know about hiring people as independent contractors versus hiring them as employees:

• IRS Publication 15-A, Employer's Supplemental Tax Guide,

• Publication 1779, Independent Contractor or Employee, and Publication 1976, Do You Qualify for Relief under Section 530?

These publications and Form SS-8 are available on the IRS Web site or by calling the IRS at 800-829-3676

(800-TAX-FORM).

IRS, STATES CRACKING DOWN ON INDEPENDENT CONTRACTOR STATUS

The Internal Revenue Service and state equivalent agencies across the country are on a beefed up hunt for employers and employees falsely or mistakenly using or selling their services as independent contractors.

According to the Associated Press, the practice of trimming payroll costs by changing an employee’s status to an independent contractor “costs governments billions in lost revenue and can leave workers high and dry when they are hurt at work or are left jobless. By designating workers as independent contractors businesses can save as much as 30% of payroll.”

As with any such dragnet, legitimate independent contractors can become ensnared. The numbers make this an almost certainty. According to The Wall Street Journal “How to succeed in the age of going solo,” Feb. 8, “Today, in fact, 20% to 30% of U.S. workers are operating as consultants, freelancers, free agents, contractors or micropreneurs. Current projections see the number only rising in coming years.”

In an article for USA Today business writer Rhonda Abrams says, “The main issue the IRS uses to determine employee status is who ‘controls’ the worker.' Abrams lists three areas the federal agency keys on: behavioral, type of relationship, and financial.

The IRS offers 10 tips on determining whether the people working for you are really independent contractors or employees. NFIB/North Dakota members wishing to know even more about the issue will have to travel out of state and visit the Montana Department of Labor & Industry’s Web site. Montana is one of just a handful of states that has actively cracked down on illicit independent contracting status. Prior to a 2006 law there were 33,000 independent contractors in Montana. When independent contractors were required to purchase a two year license and submit necessary documentation their numbers dropped by half. On the “New IC Laws Explained” page of the department’s Web site, The AB Test section of the story will tell members what Montana looks for. Other helpful links can be found there as well.

While North Dakota has not gone as far as Montana in registering and licensing its independent contractors it is expected to be forthcoming,as states look for any potential revenue source during this recession.

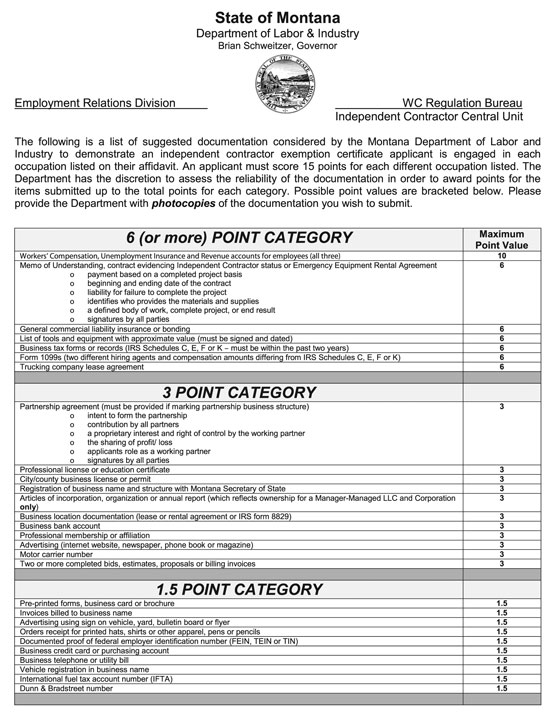

The State of Montana 15 Point Independent Contractor Test

Click to enlarge list image