THE DIFFERENCES BETWEEN CONDOMINIUMS AND CO-OPERATIVE APARTMENTS

HOW TO BUY AND SELL YOUR PROPERTY

New York State Real Estate Board

Photos: Elena Michaels

THE DIFFERENCES BETWEEN CONDOMINIUMS AND CO-OPERATIVE APARTMENTS

Condominiums

Owning a condominium is just like owning any other kind of home with one difference. In a condominium, a purchaser owns the apartment plus a percentage of the common areas of the building. The purchaser takes title by deed which is recorded in the County Clerk's office.

Condominium boards often require a down payment of at least 10%. The condominium owner pays monthly "common charges" which are his or her share of the general upkeep of the building – i.e. employee salaries, fuel, insurance, management fees, etc.

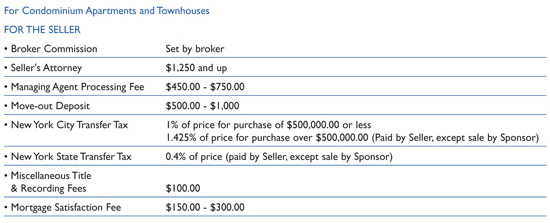

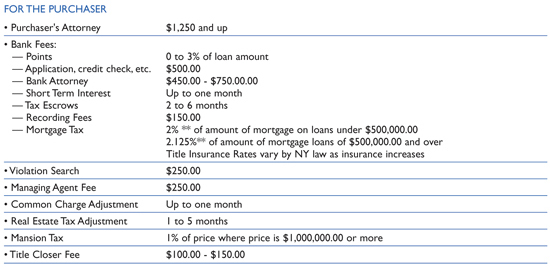

The owner pays the real estate taxes allocated to the apartment. No board interview is required of a purchaser and there are often no limitations on the amount of money you can borrow to finance the apartment. You can sell your apartment to whomever you please, at any time, with only the condominium board's Right of First Refusal. The closing costs for purchasing a condominium are higher than for a co-operative.

In a co-op, the cooperative apartment corporation owns the entire building including all the apartments. The corporation issues shares of its stock which are allocated to each apartment depending on the size and features.

Co-operatives

When you purchase a co-op you are actually purchasing shares in the apartment corporation. The corporation usually has a mortgage on the entire building. However each purchaser may have a separate loan for the purchase of his or her apartment.

The apartment corporation establishes the amount of financing allowable on apartments purchased in the building. The range is literally from all cash (i.e. no financing allowed), to 90% financing.

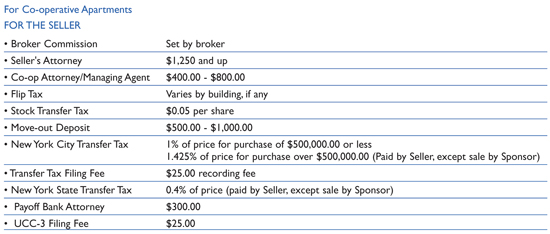

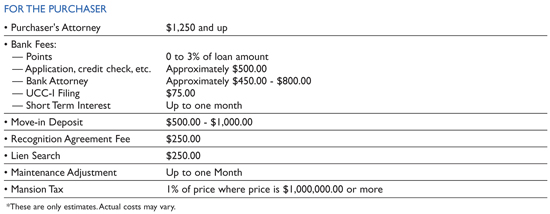

In a co-op, the purchaser pays monthly maintenance charges based on his or her share of the underlying mortgage and real estate taxes of the entire building as well as expenses for general upkeep, salaries, fuel, etc. Monthly maintenance charges for co-ops are generally higher than for condominiums. The portion of the maintenance charge comprised of mortgage interest is tax deductible.

A major difference between co-op and condominium ownership is that in a co-op your ownership is subject to approval by a Board of Directors. This Board is elected from among the shareholders. The Board's job is to conduct the business of the Apartment Corporation and oversee the management of the building usually with the assistance of a Managing Agent. The Board may impose limits on the amount of money you need to finance your apartment as well as restrictions on sub-letting, etc. You cannot sell a co-op without the board's approval of the prospective buyer.

The Purchasing Process

The purchasing process in New York City is a complex series of events. It is difficult to estimate how long the process will take from acceptance of the bid to closing. Under normal circumstances a closing can take place in four to twelve weeks.

For a condominium closing, the purchaser must first obtain a loan commitment unless they are paying cash. Then the seller must receive a Waiver of the Right of First Refusal from the Condominium Association's board. For a co-op closing, the purchaser must obtain a loan commitment, and finally, approval of the sale by the co-op's Board of Directors after a personal interview. Your REBNY member broker will be able to give you an estimate of closing time based on his/her experience dealing with the managing agent and board of the building you have chosen.

The Offer to Purchase

Once you have determined the apartment you want to purchase, your REBNY member broker will help you negotiate an accepted offer. Your offer should include the price you will pay, the percentage of the price you will finance, if so, the inclusions or exclusions of any personal property and your desired closing date. Remember, until a contract is signed by and delivered to both parties you do not have a deal.

Hiring an Attorney

New York City has complex real estate laws. Your REBNY member broker can assist you in hiring a local real estate attorney. The lawyer will initially perform a "due diligence" review of the underlying documents for a co-op or condo to determine, prior to your signing a contract, whether there are any legal or financial problems with the building where the apartment is located.

For a condominium, the lawyer should review the offering plan, all the amendments, the by-laws, the house rules, the financial statements and the title report. For a co-op, the lawyer should review the offering plan and all the amendments, the by-laws and the house rules, the financial statements and the proprietary lease. In addition, the attorney should review the corporate minutes of the cooperative at the managing agent's office. Reviewing the minutes will provide insight into any current or future problems in the building and reveal if there are major expenses to be incurred by the co-op corporation and its shareholders.

The Contract of Sale

Once an offer has been accepted, the seller's real estate attorney will prepare the contract of sale and forward it to your real estate attorney. At this point, you should inform your attorney of any particular terms of the transaction or any special circumstances you think may be important. The attorney will make any changes or additions to the contract that may be necessary to protect your interests.

After the contract is finalized the lawyer should meet with you to explain your rights and obligations under the terms of the contract. You will sign three or four copies of the contract and will provide a personal check payable to the order of the seller's attorney (usually equal to 10% of the purchased price), representing the down payment. The contracts and the down payment check are then delivered to the seller's attorney.

The sellers' attorney will hold your down payment in his trust or escrow account until closing. Thereafter, the seller signs the contract, the seller's attorney signs the contract acknowledging receipt of the down payment and two fully executed copies are returned to your attorney. Your attorney will deliver one original contract to you and a copy to your lender or mortgage broker. After receiving the signed contract promptly submit your final mortgage application if you have not already done so.

Obtaining a Loan

Before you even start your apartment quest your REBNY member broker can put you in contact with a mortgage broker or lender to determine your qualifications and obtain the loan you want. You can apply for a loan directly through a lender (e.g. a bank) or use the services of a mortgage broker.

The Mortgage Broker

Residential mortgage brokers are regulated by the New York State Banking Department. Mortgage brokers negotiate, originate and process residential real estate loans on behalf of the borrower. A mortgage broker does not actually lend money to prospective purchasers. Instead, he/she will arrange for a loan through an institutional lender on behalf of the purchaser.

A lender's decision to make a loan is usually based upon the following factors:

To verify this information the lender will:

When obtaining a loan on a condo or co-op apartment, the mortgage broker or lender will need to make sure the building is in good financial condition. Therefore, when applying for a loan, it is a good idea to obtain the building's financial statements for the last two years.

It normally takes three to six weeks to obtain a written loan commitment. A "commitment" is the lender's written agreement to lend you money to buy the apartment. Once the loan commitment has been issued your attorney should review it. If everything is in order sign the commitment and return it to the lender or mortgage broker as directed.

Co-Op Board Approval

The sale of a co-op is conditional upon the co-op board approving the purchaser unless you are purchasing directly from the sponsor. The contract provides that you promptly submit your application for board approval after issuance of a financing commitment, if any. You must cooperate with the co-op board requests and provide any documentation it requires to approve your purchase.

Each co-op board establishes the financial requirements for prospective purchasers in their building. In addition, co-op boards set financial limitations on the amount of money a prospective purchaser may borrow in order to conclude the transaction. For example, many co-ops allow a purchaser to finance only 50%-75% of the purchase price.

The Co-Op Closing

The closing is ordinarily held at the office of the Managing Agent for the apartment corporation. It is attended by you, your attorney, the seller, the seller's attorney, the lender's attorney, a representative from the managing agent's office and the real estate agents involved. At the closing, you will first sign all the documents necessary to secure interest in the apartment. These documents include a Security Agreement, Promissory Note, a Stock Power and an Assignment of Lease.

Then you will sign and receive all documents to convey the co-op apartment to you, including stock certificates, the proprietary lease and consent. Checks, representing the balance of the purchase price and adjustments, are exchanged for the keys.

Condominium Board Approval

The sale of a condominium is conditional upon the Board of Managers' Waiver of the Right of First Refusal approving the purchaser unless you are purchasing directly from the developer. Your purchase contract provides that you promptly submit your application for board approval after issuance of a financing commitment, if any. You must cooperate with the condo board requests and provide any documentation it requires to issue the waiver.

The Condominium Closing

The closing is ordinarily held at the office of the lender's attorney unless it is a developer sale. In the latter case it is held at the developer's attorney's office. The condo closing is attended by you, your attorney, the seller, the seller's attorney, the lender's attorney, the title company closer and the real estate agents involved.

At the closing you will first sign all documents necessary to put a first mortgage on the apartment. These documents include a Mortgage and a Promissory Note. Then you will sign and receive all documents to convey the condo apartment to you including a deed, title report and unit power of attorney. Checks representing the balance of the purchase price and adjustments are exchanged for the keys and you pay all appropriate taxes and title charges.

Tax Advantages of Home Ownership

The current federal and state tax laws favor and generously reward home ownership. There are numerous ways a condominium, co-op or townhouse owner will save on taxes while building equity in their property.

All of the interest paid toward a home mortgage is fully tax deductible. For example: If the total mortgage payment is $3,000 per month (where in the early stages of your mortgage most of the payment is interest), assuming the interest is $36,000 per year ($3,000 x 12), and you are in the 28% tax bracket, a $36,000 deduction means a federal tax saving of over $10,000. Meanwhile, the property continues to appreciate in value as your home grows in value. All the money you pay in real estate tax is fully deductible.

When your apartment is your principal residence and you decide to sell, you may exclude up to $250,000 of your total gain, $500,000 if you are married and file a joint return. This exclusion is allowed each time a taxpayer sells or exchanges a principal residence although the exclusion generally may not be claimed more frequently than once every two years.

As you can see, the deduction from taxable income, and the deferral of capital gains when you sell are important considerations when you weigh the benefits of owning against renting in Manhattan.

Valuing Your Property

It is knowledge of the current real estate market, including historical sales and current availability of similar properties, that allows your broker to accurately price your home. As a marketing expert, your broker will even offer suggestions as to how you might enhance the appearance of your home to help achieve the best sales price possible.

Marketing Your Property

Your REBNY member broker will launch an array of strategies to expose your home to prospective buyers.

Depending on the property the broker may:

Selling Your Property

Your REBNY member agent is familiar with every aspect of your property. He or she will verify necessary information with managing agents. He/she will usually be present every time your property is shown, ready to highlight everything that makes your residence special. Your agent involves you only as necessary while shielding you from the endless details inherent in the selling process. He/she will answer all inquiries, screen all prospective buyers, and advise you as offers are made.

Closing the Sale

Once an initial offer is made, your REBNY member agent will begin negotiations on your behalf. He/she will handle all aspects of the transaction with authority and help you obtain the highest possible price for your investment. In addition, because your broker knows the real estate business, as well as the specific players involved in your deal, he/she can make your transaction proceed smoothly and rapidly as he/she negotiates and communicates with a myriad of other professionals: attorneys, mortgage brokers/bankers, appraisers, managing agents, co-op board members and settlement personnel.

Building Terms

Luxury doorman building

Usually refers to new construction or apartment buildings that were built within the past twenty or so years. These buildings tend to be condominiums, typically stand twenty to forty or more stories tall and provide concierge services. Many have health clubs and/or swimming pools.

Pre-war building

By definition, a building built before World War II. These buildings are usually ten to twenty stories tall and are sought after for their larger rooms, fireplaces, hardwood floors and higher ceilings. They may or may not provide a doorman.

Post-war building

These buildings were built between the late 1940s and the late 1970s. They are generally hi-rise and most have doormen.

Elevator building

This term usually describes a 6 to 20 stories tall non-doorman building which may be pre-war or post-war. Elevator buildings usually have an intercom or video security system.

Walk-up building

This is the least expensive type of housing in New York City and the quality can vary widely. Usually these are 4 to 5 story buildings with no doorman and no elevator. They were originally constructed as multi-family dwellings and do not exude the charm or elegance of brownstones or town homes.

Brownstone or Townhouse

Four- to six-story buildings built in the 1800s to early 1900. These can be single family houses or may have been converted over the years into multiple apartments. They are prized for their charm and elegance. In almost all cases these buildings do not have a doorman.

Loft apartment

Former commercial or industrial buildings that have been converted into apartments. These buildings almost never provide a doorman and usually consist of vast spaces with high ceilings.

Studio

One or two rooms with combined living and sleeping areas.

Alcove studio

A one or two room apartment with a separate alcove which can be used as a sleeping or dining area. Alcoves usually adjoin the living room space of the apartment, are generally less than 100 square feet and can sometimes be walled off to create an additional bedroom.

Junior

An apartment with an alcove off of the living room has been converted into a bedroom or dining room. For example, a Junior 4 would be a three room apartment, (living room, kitchen and bedroom), which has four rooms by using the alcove space to create an additional room.

Convertible

This is typically an apartment with an alcove adjacent to the living room that can be used to create another room by using this "flexible" space to "convert" the apartment from, for example, a one bedroom to a two bedroom.

Classic

The word "classic" is usually followed by a number indicating the number of rooms in an apartment. It is usually associated with pre-war apartments that meet criteria for numbers of rooms and design. However, a "classic" can exist in a post-war building assuming it follows the same guidelines. As an example, a "classic six " is comprised of a living room, dining room, kitchen, two bedrooms and a maid's room. A "classic seven" is comprised of a living room, dining room, kitchen, three bedrooms and a maid's room.

Loft area

This is an additional space created in apartments with very high ceilings. The loft area is constructed above the living area, accessed via a staircase or ladder and used for extra storage, sleeping or living space,e.g. an office.

Duplex

In Manhattan this refers to an apartment with two floors or on two levels and not to two apartment units.