WORKERS COMPENSATION 2011: IT'S HISTORY & DRAMATIC NATIONAL DEVELOPMENTS

![]()

![]()

Industry premiums for workers comp dropped 23 percent countrywide between 2007 and 2009 due in part to the recession, in particular the loss of jobs in the manufacturing and construction sectors, and to intense competition among workers compensation insurers for market share. On the positive side, the number of injuries reported continues to decline, with lost-time claims falling 4 percent in 2009 (and 54 percent since 1991), as the workplace becomes safer.

Workers compensation insurance covers the cost of medical care and rehabilitation for workers injured on the job. It also compensates them for lost wages and provides death benefits for their dependents if they are killed in work-related accidents, including terrorist attacks. The workers compensation system is the “exclusive remedy” for on-the-job injuries suffered by employees. As part of the social contract embedded in each state’s law, the employee gives up the right to sue the employer for injuries caused by the employer’s negligence and in return receives workers compensation benefits regardless of who or what caused the accident, as long as it happened in the workplace as a result of and in the course of workplace activities.

Workers compensation systems vary from state to state. State statutes and court decisions control many aspects, including the handling of claims, the evaluation of impairment and settlement of disputes, the amount of benefits injured workers receive and the strategies used to control costs. From 2008 to 2009 maximum income benefits for total disability increased an average 3.67 percent. The average maximum weekly benefit in 2009 is $763.16, according to the U.S. Chamber of Commerce 2009 Analysis of Workers Compensation Laws.

Workers compensation costs are one of the many factors that influence businesses to expand or relocate in a state, generating jobs. When premiums rise sharply, legislators often call for reforms.

The last round of widespread reform legislation started in the late 1980s. In general, the reforms enabled employers and insurers to better control medical care costs through coordination and oversight of the treatment plan and return-to-work process and to improve workplace safety. Some states are now approaching a crisis once again as new problems arise.

RECENT DEVELOPMENTS

State activities:

Competitive with Private Insurers |

Exclusive |

||||

| Arizona* | Kentucky | Missouri | Oregon | North Dakota | |

| California | Louisiana | Montana | Pennsylvania | Ohio | |

| Colorado | Maine | New Mexico | Rhode Island | Washington | |

| Hawaii | Maryland | New York | Texas | Wyoming** | |

| Idaho | Minnesota | Oklahoma | Utah | ||

*Scheduled to be privatized by 2013.

**Compulsory for extra hazardous operations only. Employers with nonhazardous operations may insure with the state fund or opt to go without coverage.

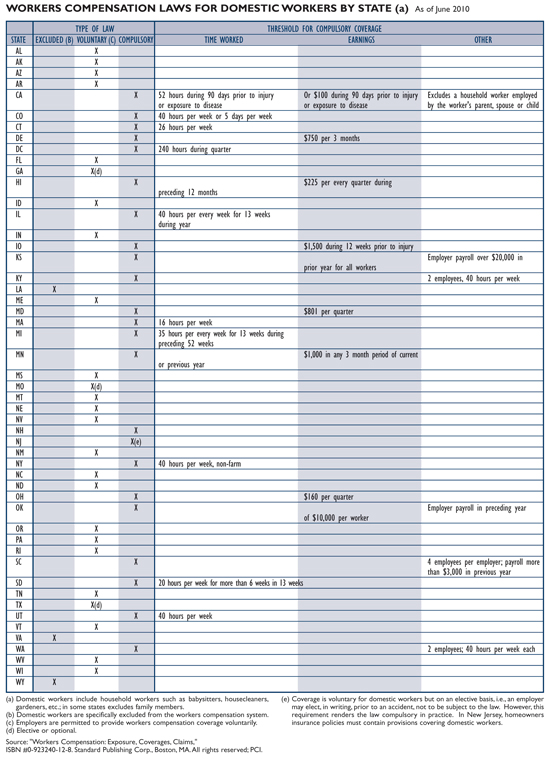

WORKERS COMPENSATION LAWS FOR DOMESTIC WORKERS BY STATE (a) As of June 2010

Click table to enlarge

BACKGROUND

The Workers Compensation Social Contract: The industrial expansion that took place in the United States during the 19th century was accompanied by a significant increase in workplace accidents. At that time, the only way injured workers could obtain compensation was to sue their employers for negligence. Proving negligence was a costly, time-consuming effort, and often the court ruled in favor of the employer. But by the early 1900s, a state-by-state pattern of legislative proposals designed to compensate injured workers had begun to emerge.

Wisconsin enacted the first permanent workers compensation insurance law in 1911 (New York had enacted a law a year earlier but it was found unconstitutional), and by 1920 all but eight states had enacted similar laws. By 1949 all states had a workers compensation system that provided compensation to workers hurt on the job, regardless of who was at fault. The costs of medical treatment and wage loss benefits were the responsibility of the employer which were paid through the workers compensation system. As part of the compromise that made the employer liable for work-related injury and disease costs regardless of fault, the employee gave up the right to sue the employer for injuries caused by the employer's negligence.

The scope of workers compensation coverage has broadened considerably since its early beginnings. In 1972, states amended their laws to meet performance standards recommended by the National Commission on State Workmen's Compensation Laws. Many states took action not only to expand benefits but also to make the coverage applicable to classifications of employees not previously covered.

However, compensation levels are not uniform. In some states benefits are still inadequate, while in others, they are overly generous. Some states were slow in adopting the National Commission's guidelines and have still not embraced the entire package of 19 recommendations published in 1972. Many states exempt employers with only a few workers (fewer than five, four or three, depending on the state) from mandatory coverage laws. A major benefits issue still to be resolved in some states is the imbalance between levels of compensation for various degrees of impairment; permanent partial disabilities tend to be overcompensated and permanent total disability under compensated.

Some coverage is provided by federal programs. For example, the Longshoremen's and Harbor Workers Compensation Act, passed in 1927 and substantially amended in 1984, provides coverage for certain maritime employees and the Federal Employees' Compensation Act protects workers hired by the U.S. government.

Employers can purchase workers compensation coverage from private insurance companies or state-run workers agencies, known as state funds. In 20 states, according to a Conning study, “Workers Compensation State funds, Evolution of a Competitive Force,” state funds compete with private insurers and in four states, the state is the sole provider of workers compensation insurance. (See list at the end of Recent Development section of this report.) Along with residual market pools, many state funds also function as the insurer of last resort for businesses that have difficulty getting coverage in the open market.

The only state in which workers compensation coverage is truly optional is Texas, where about one-third of the state’s employers are so-called nonsubscribers. In the event of a serious accident, those that opt out of the system can be sued by employees for failure to provide a safe workplace. The nonsubscribers tend to be smaller companies, but the percentage of larger companies opting out is growing. Some 25 percent of the state’s workers were employed by nonsubscribers in 2008, compared with 23 percent in 2006.

Some businesses finance their own workplace injury benefits through a system known as self-insurance. Large organizations with many employees can often estimate the cost of routine types of injuries. Self-insurance, along with large deductibles, which are in effect self-insurance, now account for more than one-third of traditional market premium. Put another way, workers compensation accounts for more than 40 percent of the alternative market, see also Captives report. Businesses that self-insure their workers compensation losses must prove that they are financially able to do so. They usually protect their assets by purchasing insurance coverage for catastrophic losses or losses in excess of a specific threshold.

About nine out of 10 people in the nation’s workforce are protected by workers compensation insurance. Laws vary by state for domestic workers, see chart.

How the System Works: Workers compensation systems are administered by the individual states, generally by commissions or boards whose responsibility it is to ensure compliance with the laws, investigate and decide disputed cases, and collect data. In most states employers are required to keep records of accidents. Accidents must be reported to the workers compensation board and to the company’s insurer within a specified number of days.

Workers compensation covers an injured worker’s medical care and attempts to cover his or her economic loss. This includes loss of earnings and the extra expenses associated with the injury. Injured workers receive all medically necessary and appropriate treatment from the first day of injury or illness and rehabilitation when the disability is severe.

To rein in expenditures and improve cost effectiveness, many states have adopted cost control measures, including treatment guidelines that spell out acceptable treatments and diagnostic tests for specific injuries such as lower back injuries and fee schedules that set maximum payment amounts to doctors for certain types of care.

Most claims are medical only, but lost-time claims, those with both medical and lost income payments, though few, consume most resources. Claims are categorized according to the degree of impairment—partial or total disability—and whether the impairment is permanent or temporary. Cash benefits can include impairment benefits and, when the impairment causes a loss of income, disability or wage loss benefits.

Impairment can be defined in several ways. Payments may be based on a schedule or list of body parts covered and the benefits paid for a loss of that part. For injuries not on the schedule, benefit payments may be calculated according to the degree of impairment or the loss of future or current earnings capacity, often using the American Medical Association’s definitions.

Most states pay benefits for the duration of the injury. But some specify a maximum number of weeks, particularly for temporary disabilities. For workers with a total disability, the benefit amount is some percentage of the worker’s weekly wage (actual or state average). Cash benefits may not be paid until after a waiting period of several days.

Costs to Employers: Costs to employers include premiums, payments made under deductibles and the benefits and administrative costs incurred by employers that self-insure or fund their own benefit program. The percentage of total compensation costs that workers compensation premiums represent fluctuates. In the mid-1950s, private sector employers paid an average 0.5 percent of payroll for workers compensation. By 1970 this figure was 1 percent, escalating steeply in the 1980s and 1990s to a record high in 1994 of 2.99 percent. The Bureau of Labor Statistics estimates that in 2009 workers compensation insurance amounted to 1.6 percent of total compensation costs. However, there is a wide variation in costs among states and industries, so that the highest rated (the inherently riskiest) groups could pay several hundred times that of the lowest rated (safest) groups, as a percentage of payroll. Also taken into account is the firm’s own safety record.

Insurance, particularly commercial insurance, is a cyclical industry marked by hard and soft markets. In 2000 as the economy expanded, premiums started rising, ushering in the hard market, when demand outstrips supply. In 2007, with a generally soft market for most types of commercial insurance and a weakening economy, premiums began dropping again. From December 2007 to mid-2009, as the recession caused payroll, the basis for computing workers compensation premiums, to drop significantly (3.6 percent) workers compensation insurers saw premiums contract. In fact, the recent recession had the most serious impact on workers compensation in terms of payroll in 60 years. In the recessions of the 1970s and 1980s, the impact was less severe because of continuous wage inflation. Inflation was not a factor in the 2007-2009 recession.

Claim Costs: As mentioned earlier, there are two components to workers compensation claims costs: payments for lost income, which are usually linked to a state’s average weekly wage, known as indemnity costs, and payments for medical care. Two decades ago, indemnity costs made up the greater part of total losses. In 1986 indemnity costs represented 55 percent of the total. By 1996 indemnity and medical had changed places, with indemnity at only 48 percent of losses. In 2008, as medical care costs continued to rise, indemnity accounted for 42 percent.

Growth in workers compensation medical costs has been much steeper than in the healthcare industry as a whole. The annual average rate of increase in workers compensation medical care costs was 3.9 percent from 1991 to 1995. Since then the rate of increase has more than doubled and, in most years, was more than twice the rate of increase in the medical Consumer Price Index (CPI). Between 2002 and 2007, the medical cost per lost-time claim—where the employee was forced to take time off work because of the injury as opposed to just seeking treatment for the injury—increased by 6.7 percent compared with an increase of 4.0 percent in the medical CPI. In 2008 workers compensation medical care costs increased by 6 percent, compared with a rise in the medical care CPI of 3.7 percent.

NCCI Holdings suggests that much of the difference between the cost of a healthcare claim and a workers compensation claim is due to the volume, duration and mix of services used by injured workers and group health claimants.

But while the size of claims (dollar amount) has been climbing due to the increasing cost of medical treatment, the number of claims filed (frequency) has been dropping steadily as insurers and their policyholders focus on safety. The frequency of lost-time claims dropped by 54.9 percent from 1991 to 2008. NCCI also attributes recent declines in the frequency of accidents to the use of robots, which reduce workers' exposure to hazardous activities; power-assisted devices that reduce physical stress, lighter and stronger materials; ergonomic designs that reduce strains; and cordless tools, which reduce the incidence of tripping over cords. Frequency declines, which first showed up among small employers are now evident also in large firms.

Insurance company financial results often report profitability in terms the combined ratio (the percentage of each premium dollar spent on claims and expenses). The combined ratio for workers compensation is reported in two different ways: by calendar year and by accident year. In 2008 the calendar year combined ratio started to deteriorate, moving from 99 in 2007 to 100 in 2008. The accident year combined ratio deteriorated more sharply going from 92 in 2007 to 101 in 2008, according to the NCCI. The accident year combined ratio hit a peak of 140 in 1999.

Calendar year results reflect claim payments and changes in reserves for accidents that happened that year or earlier. Insurance companies have to set aside reserves for accidents that have happened but where claims have not been settled. Workers compensation claims may not be settled for many years, if the accident victim needs increasingly more treatment, for example. Accident year results, in that they include only losses from a specific single year, may present a better picture of the industry's performance at a given point in time.

Reducing Costs: Workers compensation system costs are rarely static. Reforms are implemented and then, over time, one or more element in these multifaceted systems get out of balance. Soon employers and legislators complain that the cost of coverage is hurting the state’s economy by reducing its ability to compete with other states for new job-producing opportunities.

In the 1980s, with a view to increasing competition within the insurance industry in order to bring down rates, legislation was introduced in more than a dozen states to change the method of establishing rates from administered pricing, where rating organizations recommended rates that included expenses and a margin for profit, to open competition. Now insurers base their rate filings on more of their own company's specific data, rather than using industry wide figures in such areas as expenses and profit and contingency allowances. Rating organizations still provide industry wide data on "losses"—the costs associated with work-related accidents, which help small companies that lack access to large amounts of data.

More recently, states have begun to disband Second Injury Funds. Set up mostly after World War II, these funds were designed to protect employers that hire disabled workers from having to bear the full cost of the first disability when an injury that further disabled the worker occurred in their workplace. Many believe that these funds are now unnecessary in that passage of the Americans with Disabilities Act has made the protection they afford to disabled workers redundant. The Act protects injured workers from discrimination by employers. At least 10 states have repealed laws covering Second Injury Funds.

The aim of the workers compensation system is to help workers recover from work-related accidents and illnesses and to return to the workplace. A fast return to work is desirable from the employer and insurer’s viewpoint, lowering claim costs for the insurer but benefiting the worker too.

Research shows that the faster the insurer receives notice of an injury and can initiate medical treatment, the faster the injured worker recuperates and returns to work and the less likely he or she is to seek out an attorney for help in dealing with a claim. Studies also suggest that most people want to return to productive employment as soon as possible. Electronic communication has enhanced procedures to speed up the "first notice of claim" filing process to the workers compensation administrative office.

There are two important aspects to facilitating the return-to-work process. One involves getting the most effective medical care as soon as possible and reducing the emotional stress that may follow an accident. To help get medical treatment to the injured worker faster, some insurers help employers file promptly a "first notice of injury" with the state agency responsible for overseeing the workers compensation system, a step which triggers the claim process.

The other is to encourage employers to improve communications, first about the workers compensation system in advance of accidents—people who know what to expect and who receive medical attention promptly will recuperate faster and are less likely to turn to an attorney for help—and second when injured workers are off work, so that they feel that they are still part of the workplace team and are anxious to return. Insurers have also strengthened communications among all the parties involved in the case so that each knows how treatment is progressing.

Another aspect of the return-to-work process is successful reintegration into the workplace. Insurers help employers assess the injured workers’ needs and capabilities and encourage them to let workers know, in advance of any injury, that they will try to modify work activities to accommodate those who are permanently disabled.

Long absences from work can have a lasting negative impact on workers’ future employment opportunities and thus on their economic well-being. A study of injured workers in Wisconsin by the Workers Compensation Research Institute found that the duration of time off work and periods of subsequent unemployment are lower for injured workers who return to their pre-injury employer than for those who change employers.

Another factor pushing up costs in some states is the amount of attorney involvement. Workers compensation programs were originally intended to be "no-fault" systems and therefore litigation-free. Attorney fees are either set by law or subject to approval of the courts or regulator. Computations may be based on an hourly rate, a percentage of the total award, a specific percentage according to the level of the hearing on the case, or a sliding scale with percentages decreasing with the size of the award. Many states have caps on attorney fees.

Although attorney involvement boosts claim costs by 12 to 15 percent, because claimants must pay attorneys' fees there is generally no net gain in the actual benefits received. Overall, attorneys are involved in 5 to 10 percent of all workers compensation claims in most states—but in as much as 20 percent in systems where the number of disputes is high and in roughly a third of claims where the worker was injured seriously.

The involvement of an attorney does not necessarily indicate formal litigation proceedings. Sometimes, injured workers turn to attorneys to help them negotiate what they believe is a confusing and complex system. Increasingly, states are trying to make the system easier to understand and to use.

The workers compensation system plays a major role in improving workplace safety. An employer's workers compensation premium reflects the relative hazards to which workers are exposed and the employer's claim record. About one-half of states allow what is known as "schedule rating," a discount or rate credit for superior workplace safety programs.

In addition, a majority of states now provide for optional medical deductibles in workers compensation insurance policies as a cost-saving measure and, in some states, allowable deductible amounts were raised. (Deductibles reduce premiums because they lower an insurer's administrative expenses, which, for small claims, make up a disproportionately large portion of the cost of settlement.) Deductibles also encourage greater safety-consciousness on the part of the employer who must pay the deductible amount.

In some states, insurers must provide accident prevention services to employers. In others, employers are required by law to set up safety committees and other programs to deal with unsafe conditions in the workplace and assign specific responsibility for creating, monitoring or overseeing workplace safety to a governmental agency.

Some businesses are taking a more radical approach to bringing costs under control through coordination of workers compensation, healthcare and disability benefit plans. The integration of workers compensation and other employee benefit programs is a broad concept that ranges from a simple marketing approach that promises savings from using the same insurer for both coverages to programs that offer a managed care approach to the management of all types of disability, regardless of whether they are work-related.

Besides limiting overlapping programs and streamlining administration, proponents say such a change addresses the increasing difficulty of distinguishing between work- and nonwork-related injuries and illnesses, such as injuries due to repetitive motion and stress claims.

It also improves productivity since nonwork-related disabilities are managed with the same focus of getting the employees back to work as work-related cases, and at the same time addresses the potential for reporting injuries that occur outside the workplace as work-related to reduce the employee's out-of-pocket costs. Workers compensation pays for all reasonable medical treatment without deductibles and co-payments, as opposed to healthcare, where the policyholder incurs some out-of-pocket costs.

Residual Markets: Residual markets, traditionally the market of last resort, are administered by the NCCI in 29 jurisdictions. In some states, particularly where rates in the voluntary market are inadequate, the residual market provides coverage for a large portion of policyholders. In 1993 they represented about 26.5 percent of the total workers compensation market (excluding employers who are self-insured). Since that time, the NCCI has taken steps to reduce the size of the residual market by creating financial disincentives to obtain coverage from it.

Terrorism Coverage: Since the terrorist attacks of September 11, 2001, workers compensation insurers have been taking a closer look at their exposures to catastrophes, both natural and man-made. According to a report by Risk Management Solutions, if the earthquake that shook San Francisco in 1906 were to happen today, it could cause as many as 78,000 injuries, 5,000 deaths and over $7 billion in workers compensation losses.

Workers compensation claims for terrorism could cost an insurer anywhere from $300,000 to $1 million per employee, depending on the state. As a result, firms with a concentration of employees in a single building in major metropolitan areas, such as New York, or near a “trophy building” are now considered high risk, a classification that used to apply only to people in dangerous jobs such as roofing. Faced with the possibility of a huge death toll costing millions of dollars and the threat of insolvency as a result, all but the largest insurers are limiting coverage. This is forcing some employers to raise their deductibles, in effect self-insuring part of the risk, and to deal with several insurers to reduce the potential maximum loss for each.

KEY SOURCES OF ADDITIONAL INFORMATION

Issues Report, a yearly overview of the workers compensation system, National Council on Compensation Insurance.

"Property/Casualty Insurance Facts," Insurance Information Institute, annual publication.

"Analysis of Workers' Compensation Laws," U.S. Chamber of Commerce, annual publication.

Publications from the Workers Compensation Research Institute, Cambridge, MA. http://www.wcrinet.org