TAX LAW CHANGES FOR INDIVIDUALS • TAX YEAR 2005

Charitable

contributions

Definition of a child

Earned Income Credit

Electric and clean-fuel vehicles

Empowerment zone stock

Exemption amounts

Retirement savings plans

Social security & Medicare taxes

Standard deduction

Standard mileage rates

Tax rate schedules - 2005

Charitable

Contributions of Vehicles, Boats, and Aircraft

If

you donate a vehicle (including a boat or aircraft) to

a qualified organization after December 31, 2004, your deduction is

limited to the gross proceeds from its sale by the organization. This

rule applies if the claimed value of the donated vehicle is more than

$500. However, you generally can deduct its fair market value if the

organization:

- Makes

significant intervening use of the vehicle,

- Materially

improves the vehicle, or

- Transfers

the vehicle to a needy individual in direct furtherance of the donee's

charitable purpose

of relieving the poor and distressed or underprivileged who are in

need of a means of transportation.

Boats, aircraft, and other vehicles.

These

rules apply to donations of boats, aircraft, and any vehicle manufactured

mainly for use on public streets, roads, and highways.

Acknowledgement required.

If

the claimed value of the car is more than $500, you must have a written

acknowledgement of your donation from the organization and must attach

it to your return. If you do not have an acknowledgement, you cannot

deduct your contribution.

The

acknowledgement must include the following information:

- Your

name and taxpayer identification number.

- The

vehicle identification number or similar number.

- A

statement certifying the car was sold in an arm's

length transaction between unrelated parties.

- The

gross proceeds from the sale.

- A

statement that your deduction may not be more than the gross proceeds

from the sale.

- The

date of the contribution.

However,

if there was significant intervening use of or material improvement

to the car by the organization, the acknowledgement does not have to

include the information in items 3, 4, and 5 above. Instead, it must

contain a certification of the intended use of or material improvement

to the car and the intended duration of that use and a certification

that the vehicle will not be transferred in exchange for money, other

property, or services before completion of that use or improvement.

This

acknowledgement must be provided within 30 days of the sale of the car

or, if there is significant intervening use or material improvement

of the car by the organization, within 30 days of the contribution.

The

organization also must provide this information to the IRS.

Donations of inventory.

These

rules do not apply to donations of inventory. For example, these rules

do not apply if you are a car dealer who donates a car you had been

holding for sale to customers.

More information.

More

information can be found in Notice 2005-44 and the 2005 revision

of Publication 526, Charitable Contributions (to be available mid-December

2005).

Uniform Definition of a Qualifying Child

Beginning

in 2005, one definition of a ?qualifying childÇ will apply for

each of the following tax benefits.

- Dependency

exemption.

- Head

of household filing status.

- Earned

income credit (EIC).

- Child

tax credit.

- Credit

for child and dependent care expenses.

Tests To Meet

In

general, all four of the following tests must be met to claim someone

as a qualifying child.

Relationship test.

The

child must be your child (including an adopted child, stepchild, or

eligible foster child), brother, sister, stepbrother, stepsister, or

a descendent of one of these relatives.

An

adopted child includes a child lawfully placed with you for legal adoption

even if the adoption is not final.

An

eligible foster child is any child who is placed with you by an authorized

placement agency or by judgement, decree, or other order of any court

of competent jurisdiction.

Residency test.

A

child must live with you for more than half of the year. Temporary absences

for special circumstances, such as for school, vacation, medical care,

military service, or detention in a juvenile facility count as time

lived at home. A child who was born or died during the year is considered

to have lived with you for the entire year if your home was the child's

home for the entire time he or she was alive during the year. Also,

exceptions apply, in certain cases, for children of divorced or separated

parents and parents of kidnapped children.

Age test.

A

child must be under a certain age (depending on the tax benefit) to

be your qualifying child.

Dependency exemption, head of household filing status, and EIC.

For

purposes of these tax benefits, a child must be under the age of 19

at the end of the year, or under age 24 at the end of 2005 if a student,

or any age if permanently and totally disabled.

A

student is any child who, during any 5 months of the year:

- Was

enrolled as a full-time student at a school, or

- Took

a full-time, on-farm training course given by a school or a state,

county, or local government agency.

A

school includes a technical, trade, or mechanical school. It does not

include an on-the-job training course, correspondence school, or night

school.

Child tax credit.

For

purposes of the child tax credit, a child must be under the age of 17.

Credit for child and dependent care expenses.

For

purposes of the credit for child and dependent care expenses, a child

must be under the age of 13 or any age if permanently and totally disabled.

Support test.

A

child cannot have provided over half of his or her own support during

the year.

Exception.

For

purposes of the EIC only, the Support test does not apply.

Qualifying Child of More Than One Person

Sometimes

a child meets the tests to be a qualifying child of more than one person.

However, only one person can treat that child as a qualifying child.

If you and someone else (other than your spouse if filing jointly) have

the same qualifying child, you and the other person(s) can decide who

will claim the child. If you cannot agree on who will claim the child

and more than one person files a return using the same child, the IRS

may disallow one or more of the claims using the tie-breaker rule explained

in Table 1.

Table

1. When More Than One Person Files a Return Claiming the Same Qualifying

Child (Tie-Breaker Rule)

Dependency Exemption

To

claim the dependency exemption for a qualifying child, all four tests

listed earlier under Tests To Meet must be met. The child generally

must also be a U.S. citizen, U.S. national, or a resident of the United

States, Canada, or Mexico. An exception applies for certain adopted

children. If married, he or she cannot file a joint return unless the

return is filed only as a claim for refund and no tax liability would

exist for either spouse if they had filed separate returns.

A

person who used to qualify as your dependent but who is not your "qualifying

child" may still qualify as your dependent as a "qualifying

relative." To claim the dependency exemption for a qualifying relative,

the child cannot be the qualifying child of any other person and all

five dependency tests discussed under Dependency Tests in Publication

501 must be met.

Note:

If you are a dependent of another person, you cannot claim any dependents

on your return.

Head of Household Filing Status

In

general, you can use head of household filing status only if, as of

the end of the year, you were unmarried or "considered unmarried"

and you paid over half the cost of keeping up a home:

- That

was the main home for all the entire year of your

parent whom you can claim as a dependent (your parent did not have

to live with you), or

- In

which you lived for more than half of the year with either of the

following:

A. Your qualifying child (defined earlier, but without regard to

the exception for children of divorced or separated parents).

But, if your qualifying child is married at the end of the year,

see Married child below.

B. Any

other person whom you can claim as a dependent.

But

you cannot use head of household filing status for a person who is your

dependent only because:

- He

or she lived with you for the entire year, or

- You

are entitled to claim him or her as a dependent under a multiple support

agreement.

Married child.

If

your qualifying child is married at the end of the year, both of the

following must apply for the child to be your qualifying child for purposes

of head of household filing status.

- The

child cannot file a joint return unless the return is filed only as

a claim for refund and no tax liability would exist for either spouse

if they had filed separate returns.

- The

child must be a U.S. citizen, U.S. national, or a resident of the

United States, Canada, or Mexico. An exception applies for certain

adopted children.

Earned Income Credit (EIC)

You

may be able to claim the earned income credit (EIC) in 2005 if you have:

- 2

or more qualifying children and your earned income is less than $35,263

($37,263 if married filing jointly for 2005),

- 1

qualifying child and your earned income is less than $31,030 ($33,030

if married filing jointly for 2005), or

- No

qualifying children and your earned income is less than $11,750 ($13,750

if married filing jointly for 2005). For purposes of the EIC, a qualifying

child must meet the Relationship test, Residency test (without regard

to the exception for children of divorced or separated parents), and

Age test, earlier. A qualifying child does not have to meet the Support

test for purposes of the EIC. But, if your qualifying child is married

at the end of the year, see Married child next.

Married child.

A

child who is married at the end of the year is a qualifying child for

purposes of the EIC only if you can claim him or her as your dependent

(see Dependency Exemption, earlier) or this child's other parent claims

him or her as a dependent under the rules for children of divorced or

separated parents in Publication 501, Exemptions, Standard Deduction,

and Filing Information.

Child Tax Credit

You

may be able to take the child tax credit if you have a qualifying child

that meets all four of the tests listed earlier under Tests To Meet.

For additional rules that you must meet, see Publication 972, Child

Tax Credit.

Credit for Child and Dependent Care Expenses

Generally,

a qualifying person for purposes of the credit for child and dependent

care expenses is:

- Your

qualifying child (defined earlier, but without regard to the exception

for parents of kidnapped children), or

- Your

dependent or spouse who is physically or mentally incapable of caring

for himself or herself and who lived with you for more than half of

the year.

For

purposes of the credit for child and dependent care expenses, a qualifying

child and dependent are determined without regard to the exception for

children of divorced or separated parents and the child is treated as

a qualifying person only for the custodial parent.

For

additional rules that you must meet, see Publication 503, Child and

Dependent Care Expenses. However, you no longer need to meet the Keeping

Up a Home test discussed in Publication 503.

EARNED INCOME CREDIT AMOUNTS INCREASE

Earned

income amount.

The

maximum amount of income you can earn and still get the credit is higher

for 2005 than it is for 2004. You may be able to take the credit for

2005 if:

- You

have more than one qualifying child and you earn less than $35,263

($37,263 if married filing jointly),

- You

have one qualifying child and you earn less than $31,030 ($33,030

if married filing jointly), or

- You

do not have a qualifying child and you earn less than $11,750 ($13,750

if married filing jointly).

The

maximum amount of adjusted gross income (AGI) you can have and still

get the credit has also increased. You may be able to take the credit

if your AGI is less than the amount in the above list that applies to

you.

Investment income amount.

The

maximum amount of investment income you can have in 2005 and still get

the credit increases to $2,700.

Electric and Clean Fuel Vehicles

For

2005, the proposed 50% reduction of the maximum electric vehicle credit

and the clean-fuel deduction has been eliminated. You can claim the

maximum electric vehicle credit allowed for a qualified electric vehicle

you place in service in 2005.

You

can claim the maximum deduction allowed for qualified clean-fuel vehicle

or other clean-fuel property placed in service in 2005.

Section 1202 Exclusion Increased for Gain from Empowerment Zone Business

Stock

You

generally can exclude up to 50% of your gain on the sale or trade of

qualified small business stock held by you for more than 5 years. This

is called the section 1202 exclusion. Beginning in 2005, you generally

can exclude up to 60% of your gain if you meet the following additional

requirements.

- You

sell or trade stock in a corporation that qualifies as an empowerment

zone business during substantially all of the time you held the stock.

- You

acquired the stock after December 21, 2000.

Condition

(1) will still be met if the corporation ceased to qualify after the

5-year period that begins on the date you acquired the stock. However,

the gain that qualifies for the 60% exclusion cannot be more than the

gain you would have had if you had sold the stock on the date the corporation

ceased to qualify.

The

part of the gain that is included in income is a 28% rate gain. See

Capital Gain Tax Rates and Section 1202 Exclusion in chapter 4 of Publication

550, Investment Income and Expenses.

For

more information about empowerment zone businesses, see Publication

954, Tax Incentives for Distressed Communities.

Exemption Amount Increased

The

amount you can deduct for each exemption has increased from $3,100 in

2004 to $3,200 in 2005.

You

lose all or part of the benefit of your exemptions if your adjusted

gross income is above a certain amount. The amount at which the phaseout

begins depends on your filing status.

For

2005, the phaseout begins at:

- $109,475

for married persons filing separately,

- $145,950

for single individuals,

- $182,450

for heads of household, and

- $218,950

for married persons filing jointly or qualifying widow(er)s.

If

your adjusted gross income is above the amount for your filing status,

use the Deduction for Exemptions Worksheet in the Form 1040 instructions

to figure the amount you can deduct for exemptions.

Retirement Savings Plans

Traditional

IRA income limits. If you have a traditional individual retirement account

(IRA) and are covered by a retirement plan at work, the amount of income

you can have and not be affected by the deduction phaseout increases.

The amounts vary depending on filing status.

Limit

on elective deferrals. The maximum amount of elective deferrals under

a salary reduction agreement that can be contributed to a qualified

plan increases to $14,000 ($18,000 if you are age 50 or over). However,

for a SIMPLE plan, the amount increases to $10,000 ($12,000 if you are

age 50 or over).

IRA

deduction expanded. The amount you, and your spouse if filing jointly,

may be able to deduct as an IRA contribution will increase to $4,000

($4,500 if age 50 or older at the end of 2005).

Social Security and Medicare Taxes

For

2005, the employer and employee will continue to pay:

- 6.2%

each for social security tax (old-age, survivors, and disability insurance),

and

- 1.45%

each for Medicare tax (hospital insurance).

Wage

limits. For social security tax, the maximum amount of 2005 wages subject

to the tax is $90,000. For Medicare tax, all covered 2005 wages are

subject to the tax.

Standard Deduction Amount Increased

The

standard deduction for taxpayers who do not itemize deductions on Schedule

A of Form 1040 is, in most cases, higher for 2005 than it was for 2004.

The amount depends on your filing status, whether you are 65 or older

or blind, and whether an exemption can be claimed for you by another

taxpayer.

The

basic standard deduction amounts for 2005 are:

- Head

of household ‹ $7,300

- Married

taxpayers filing jointly and qualifying widow(er)s

‹ $10,000

- Married

taxpayers filing separately ‹ $5,000

- Single

‹ $5,000

The

standard deduction amount for an individual who may be claimed as a

dependent by another taxpayer may not exceed the greater of $800 or

the sum of $250 and the individual's earned income.

Standard Mileage Rates

For

tax years beginning in 2005, the allowable deductions for the standard

mileage rate for the period January 1, 2005, through August 31, 2005,

are as follows:

- Business

miles. The standard mileage rate for the cost of operating your car

increases to 40.5 cents a mile for all business miles driven.

- Charitable

services. The standard mileage rate allowed for use of your car when

you use your car to provide charitable services to a charitable organization

is 14 cents a mile.

- Charitable

services ‹ Hurricane Katrina relief services. If you used your

vehicle in giving services to a charitable organization to provide

relief related to Hurricane Katrina, the standard mileage rate

allowed for use of your car is 29 cents a mile for miles driven after

August 24, 2005, and before September 1, 2005.

- Medical

reasons. The standard mileage rate allowed for use of your car for

medical reasons is 15 cents a mile.

- Moving.

The standard mileage rate for determining moving expenses is 15 cents

a mile.

The

allowable deductions for the standard mileage rate for the period September

1, 2005, through December 31, 2005, are as follows:

- Business

miles. The standard mileage rate for the cost of operating your car

increases to 48.5 cents a mile for all business miles driven.

- Charitable

services. The standard mileage rate allowed for use of your car when

you use your car to provide charitable services to a charitable organization

remains at 14 cents a mile.

- Charitable

services. Hurricane Katrina relief services. If you used your vehicle in

giving services to a charitable organization to provide relief related

to Hurricane Katrina, the standard mileage rate allowed for use

of your car is 34 cents a mile.

- Medical

reasons. The standard mileage rate allowed for use of your car for

medical reasons is 22 cents a mile.

- Moving.

The standard mileage rate for determining moving expenses is 22 cents

a mile.

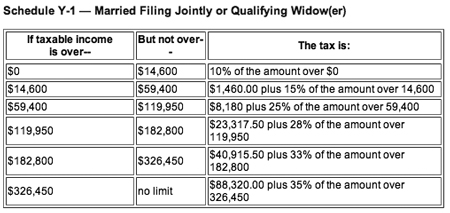

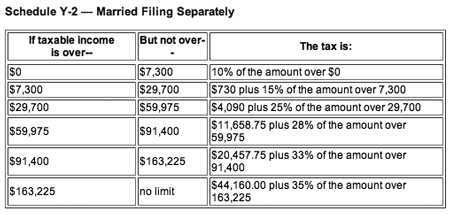

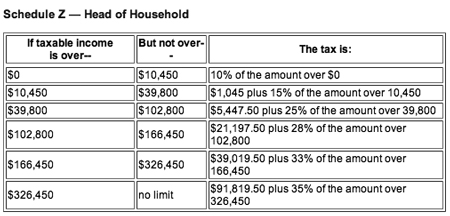

2005 Tax Rate Schedules

Note:

These tax rate schedules are provided so that you can compute your estimated

tax for 2005. To compute your actual income tax, please see the instructions

for 2005 Form 1040, 1040A, or 1040EZ as appropriate when they are available.

© 2015 TLC Magazine Online, Inc. |