|

|

PRIVATE PASSENGER AUTO PREMIUM RATING ERROR: INDUSTRY ESTIMATES OF 2004The 2004 National Premium Audits represented in this article were assembled and evaluated in 2005 Quality Planning Corporation

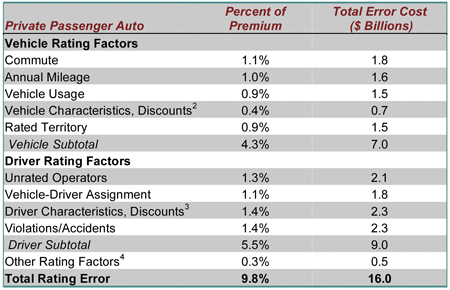

In 2004, the Private Passenger Auto Insurance industry lost over $16 billion due to premium rating error. The estimate is based on nationwide premium audits conducted by Quality Planning Corporation. Premium rating error represents 9.8% of a total $163 billion in personal auto premium written. This report aggregates and summarizes audit results of over 16 million policies from 18 major carriers. The sample includes substandard to preferred books of business, all distribution channels, and national and regional carriers.1 Sample results were weighted to reflect the total national private passenger auto line.

The audits found substantial rating error exists in all common factors used to determine auto premium. Table 1 presents losses by rating factor.

Rating error costs were found to vary greatly by individual insurer. The amount and kind of rating error varies by many factors including: characteristics of the book of business, geographic location, distribution channels, rating plan, systems history, regulatory environment, relations with sales agents, and underwriting standards.

Direct

Premium Losses

Rating error causes honest insureds to subsidize dishonest insureds. It results in low risk drivers subsidizing high-risk drivers. It results in those who drive low mileages subsidizing those with high mileages. Similarly, the majority of sales agents who work to accurately determine premium have a strong interest in rating integrity. In the absence of meaningful controls, the honest agent is placed at a competitive disadvantage by the minority of agents willing to mis-rate a policy to close a sale.

Rating error can be introduced at all stages of the underwriting cycle: sales, underwriting, policy servicing and renewal. While significant error occurs at initial application, our analysis has shown the majority of rating error arises through changes in rating factors over time. Americans lead dynamic lives. Every hour there are 203 marriages and 109 divorces. Every hour 4,900 Americans move and 7,100 change jobs. Every hour there are 12,400 vehicles registered of which 2,200 are new. Every hour there are 160 drunk driving arrests, five traffic fatalities and over 2,000 auto insurance claims paid. Every hour 550 new drivers licenses are issued.5 All of this makes personal auto insurance risk management a rapidly moving target. The risk profile of auto policies is constantly changing. Consider job changes. The time is long passed when a worker got a job soon out of school and stayed with the same company throughout their career. In fact, the average worker has held 10 jobs by the age of 36. Overall, 25 percent of workers change jobs each year. Individual job change is likely to be associated with changes in vehicle usage, commute distance, and annual mileage. Unlike homeowners insurance, in personal auto the most basic facts of the policy change frequently. Forty-eight percent of household auto policies experience a change of vehicles or drivers each year. Nearly one-third of households replace vehicles each year. These changes, in turn, are associated with changes in vehicle-driver assignment, annual mileage, commute, and other rating factors. Insurers provide their policyholders with multiple methods to report changes. Not surprisingly, many changes are not reported. Policyholders are significantly more likely to report life changes that reduce auto premium than report changes that increase premium. For example, we have found policyholders are more than five times more likely to report mid-term mileage changes that lower annual premium than to report mileage changes that raise premium. Everyday, in the course of conducting premium audits, we find examples of younger drivers who retain a policy address of their parents in the suburbs long after they have moved to higher rated territories in central cities.

Quality Planning Corporation, the Rating Integrity Solutions Company, was founded in 1985 and is headquartered in San Francisco. A member of the ISO family of companies, QPC is focused exclusively on providing decision integrity solutions to the insurance industry. QPC works with insurance companies to identify areas of significant premium leakage using sophisticated database management, statistical analysis and modeling, customized survey design, and highly targeted customer interaction. For more information, visit www.qualityplanning.com

The 2003 Premium Rating Error Report aggregates and summarizes audit results of over 14 million policies from 16 major carriers. The sample includes substandard to preferred books of business, all distribution channels, and national and regional carriers.6 Sample results were weighted to reflect the total national private passenger. Two primary methods were used to develop the estimates of rating error: Statistical Risk Estimators and Direct Measures. Statistical Risk Estimators: The first method we employ to estimate rating error is to compare the “expected distribution” of rating factors to the “rated distribution”. In the case of annual mileage the “expected distribution” is the distribution given the characteristics of policies written. We “expect” the average new Ferrari to be driven an average of 3,500 miles per year and the average new Chevy cargo van to be driven more than 20,000 miles. Based on numerous studies of vehicle use patterns we have estimated and validated equations which develop an “expected mileage” based on vehicle make, model, and year; number of vehicles in the household; garaging ZIP code; number of drivers in the household; age and occupation of driver and so on. Actual odometer reading data from over 80 million vehicles was used in developing the statistical models. For every vehicle insured, “expected mileage” is compared to “reported mileage” to detect any patterns of systematic error. Direct Measures: The second method we use to estimate rating error is direct measurement. For over a million vehicles in the sample we had data for multiple odometer readings to evaluate actual annual mileage. In addition, for multiple carriers, we interviewed overnearly one million insureds concerning their vehicle usage patterns and annual mileage. Results of the odometer and interview data, in turn, were used to validate and refine the statistical models. Statistical and direct measures were combined for each carrier in the sample and contrasted with rated values. These were then consolidated for this industry report.

© 2015 TLC Magazine Online, Inc. |