CREDIT SCORES CAUSE 65% FLUCTUATION IN AUTO INSURANCE PREMIUMS

by John S Kiernan

2014 Car Insurance by Credit Score Report

Everyone knows that auto insurance is mandatory (except in New Hampshire). Furthermore, we know that our credit scores dictate the types of loans and credit cards for which we can garner approval. But when it comes to the connection between credit scores and car insurance, most of us are in the dark.

With that in mind, WalletHub set out to determine:

- how transparent insurance companies are in disclosing the use of credit data in underwriting decisions;

- how transparent they are about the source of their credit data; and

- the extent to which credit data impacts insurance policies across the 50 states and the District of Columbia.

In evaluating the importance of credit data to insurance underwriting, WalletHub obtained quotes from five of the largest auto insurance providers in the country for two hypothetical consumers who are identical save for the fact that one has excellent credit while the other has no credit. This allowed us to isolate for the role of credit in insurance policy pricing.

It is important to note that the exact credit based pricing fluctuations discussed throughout the report may not hold true for all consumers given the multitude of other factors that contribute to the insurance policies each of us are extended. In other words, the fact that credit scores impact insurance premiums to a significant extent should be the main takeaway for consumers rather than the exact amount of the impact.

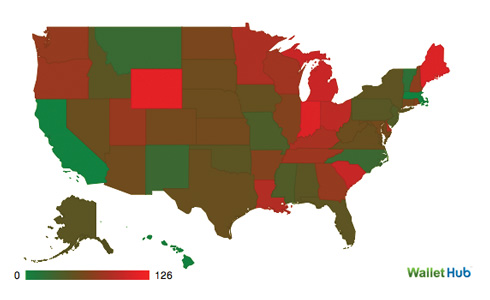

States Where Credit Data is Most & Least Significant

*All numbers in the above chart are percentages.

Key Findings

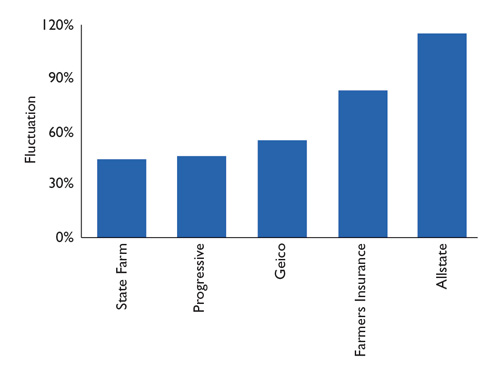

- Allstate appears to be the company that relies on credit data the most, with the WalletHub Scenario revealing a 116% fluctuation in premiums between a consumer with excellent credit and a consumer with no credit.

- State Farm seems to rely on credit data the least, displaying a 45% premium fluctuation

- In the average state, there is a 65% differential in the cost of car insurance premiums for a person with an excellent credit score and a person with no credit history.

- Credit data has the least impact on insurance premiums in Vermont (18% fluctuation) and the greatest impact in the District of Columbia (126% fluctuation).

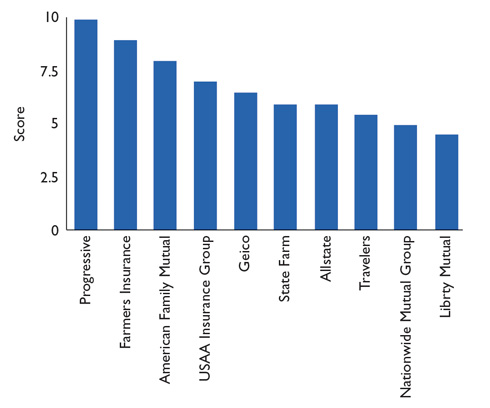

- Progressive is the most transparent about both the use of credit data in quote generation and the source of that credit data, scoring the maximum 10 points in this category.

- In contrast, Liberty Mutual – the lowest scoring provider – obtained a score of only 4.5.

- Of the five major insurance providers that WalletHub examined, Geico uses credit data in the fewest states (42).

Average Premium Fluctuation by Company

*Averages reflect quotes for the WalletHub Scenario. States in which credit score is not used have been excluded.

Insurance Provider Transparency Ratings

Company Transparency Score*

*For information about how transparency was evaluated, see the Methodology section of this report.

Methodology

In order to determine the impact of consumer credit data on car insurance premiums, we collected premium quotes from the websites of five of the largest insurance providers in the United States, based on the total number of insurance premiums issued in the third quarter of 2013, according to SNL Financial. In light of the fact that insurers use numerous

variables in pricing their policies, we obtained quotes for two hypothetical consumers, identical save only for their credit history. More specifically, one consumer has excellent credit while the other has no credit history.

Our base case, also referred to as the “WalletHub Scenario” in this report, assumes the following details about the driver and the automobile:

Base Case - Experienced Male Driver

|

|

Licensed: 20 Years / Age: 36 Years

|

Marital Status and Gender: Single Male Employment Status/

Profession: Unemployed

|

Membership in organization: No membership

|

Commute: 20 miles each way

|

|

Vehicle: 2008 Honda Accord LX, 4 cyl., Sedan

|

Assume driver side air bag, standard performance, no anti-theft device.

|

2008 Honda Accord |

|

- coverage of $50,000 for injury/death to one person

|

- $100,000 for injury/death to more than one person and $50,000 for damage to property

|

- medical coverage of $1,000 (MED)

|

- coverage for collision with uninsured motorist of $30,000

|

- collision with underinsured motorist of $60,000 (UMUND)

|

- $1,000 collateral coverage (COLL)

|

- $1,000 comprehensive coverage (COMP)

|

© 2014 TLC Magazine Online, Inc. |