|

||||||||||||||||||||

ARE WE RUNNING OUT OF OIL?by

Jean Statler The

Harris Report, Volume I, Issue I, May 2006

Introduction There is a high degree of controversy surrounding America’s use of energy to provide transportation, heat and cool homes and businesses, and spur economic activity and job creation. There are some facts which are largely misunderstood by the American people. In fact, fewer than one in three US adults surveyed consider themselves informed (20%) or very informed (11%) about energy issues. As a result, public opinion about the energy industry often tends to be based on inaccurate or incomplete information. This report, based on the results from the January, 2006 edition of The Harris Poll®, is designed to explore what drives consumer opinion about energy broadly, highlight gaps in knowledge among the general population, and provide a baseline against which attitudes over time. It also includes a short essay called ‘So What? The Implications of This Research’ on what we believe these survey data mean for the future.

In recent months, the US energy industry has been the subject of much media attention, mainly due to rising energy prices. Industries in the energy sector, including coal, nuclear, electric, natural gas and especially oil, are under the microscope. This increased scrutiny has led to the widespread public perception that the main driving force in energy prices is increasing energy company profits. When asked what factors have the greatest influence in determining energy prices, the majority of American adults (55%) cite “profits to the energy companies.” At the same time, many people are aware that demand for energy also plays a critical role in determining price. More than one-third (38%) of the general adult public cites demand as one of the three most influential factors in determining energy prices. Interesting differences in perceptions emerge among different demographic groups. For example, younger Americans do not place as much emphasis on company profits as do older Americans. About one-third (34%) of Echo Boomers (ages 18 to 27) believe profits are a major influencing factor, while older age groups such as Baby Boomers (ages 45 to 58) and Matures (ages 59 and over) are much more likely (63% and 65%, respectively) to believe company profits play a role in dictating price. Another interesting demographic difference is found in education. College graduates are more likely (49%) to assign weight to the demand for energy as a factor in price than those who’ve attained lower levels of eduction (35%). Although our question asked about energy in general, the public appears to be focused on the price of gasoline when asked what factors influence energy prices. Rounding out the top five factors mentioned, after profits and demand, are OPEC (33%), crude oil prices (32%) and political instability in oil rich nations (29%). To further examine attitudes toward oil company profits, we asked respondents how much they believe the cost of a gallon of gas would decrease if the company mark-up for profit was eliminated. One-third (33%) say the price of a gallon would decrease between 16 and 30 percent, while another third (34%) think it would go down by 31 to 60 percent. The median guess was a decrease of 31 percent.

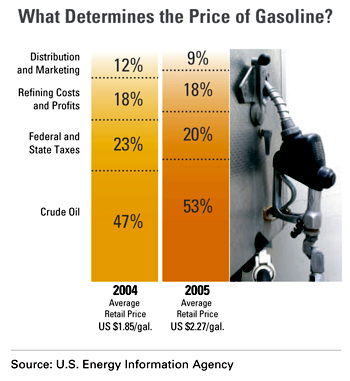

According to the Energy Information Administration (EIA), the price at the pump is a function of four factors: 1) the price of crude oil determined on the open global market, 2) federal and state taxes, 3) refining costs and profits, and 4) distribution and retailing. While some members of the American public recognize the influence of the price of crude oil (32% cite this as a major factor in determining price) and federal state and local taxes (24% name taxes as a major component of price), fewer are aware of the impact the cost of harvesting and preparing fuel for our consumption has on prices at the pump. The graphic below details the components of gasoline prices, and how those changed from 2004 to 2005. The cost of crude oil is, by a large margin, the biggest factor in determining price at the pump. On the other hand, profits, even when combined with refining costs, play a much smaller role in determining gasoline prices.

In late 2005, the Federal Trade Commission (FTC) released its report: Gasoline Price Changes: The Dynamics of Supply, Demand and Competition, which supports the EIA analysis. One of the report’s conclusions is that “over the past 20 years, changes in the price of crude oil have led to 85 percent of the changes in the retail price of gasoline in the United States, while other important factors have included increasing demand, supply restrictions, and federal, state and local regulations such as ‘clean fuel’ requirements and taxes.” (This report is available at the FTC website, www.ftc.gov.) Since retail gasoline prices are driven mostly by the cost of crude oil, we can’t fully understand gas prices without understanding the dynamics of crude oil pricing. That is clearly beyond the scope of this article, but we can point to a couple of factors affecting those prices that are not commonly understood by the public: First, world energy markets are being radically reshaped by the substantial and growing energy demand of developing nations. The US Energy Information Agency has tracked how world consumption of energy is beginning to shift from established industrialized countries to fuel emerging countries, such as China and India. Increasing demand around the globe affects the price of crude oil for everybody, including US refiners. Another thing most people do not realize is that only a fraction of the world’s crude oil production is controlled by investor-owned public companies. After the oil embargo and supply disruptions of the 1970s and early 1980s, most foreign governments nationalized their oil industries, including their reserves. Today, 77 percent of world oil reserves are owned by national oil companies and only six percent are held by investor-owned oil and natural gas companies. That means that US and other oil companies have virtually no control of crude oil prices. In a recent speech, Red Cavaney, President and CEO of the American Petroleum Institute, a trade association, talked about the implications of the phenomenon of nationalization in this critical global and commodity market. He said investor-owned oil and natural gas companies (the five largest known to Americans as ExxonMobil, Chevron, ConocoPhillips, BP, and Shell) scaled up to better compete “within this new world by creating large scale efficiencies, greater technological prowess and substantially broader competitive access to capital markets in order to address the competition from these national oil companies, such as those of Saudi Arabia, Russia, Venezuela, China, and others.” The rationale for this scaling up, Cavaney went on to say, “was missed by most observers—both in and out of government. Some observers, still in the dark on this necessary evolution, now view the industry in exaggerated, negative terms; as too large, too powerful, and not deserving of its earnings.” Many people in the public and the media believe that oil companies have gotten too big and they are making too much money. Industry critics claim it all boils down to greed. But oil companies counter that they are big for a reason, namely, to survive in the global economy, and that rising profits are the result, rather than the cause of higher gasoline prices.

Americans feeling the pinch of high gasoline prices can’t be blamed for having a “sky is falling” mentality. The notion that the world is running out of oil is a widely held belief that affects how consumers feel about a host of energy related issues, from confidence in the industry to perceptions about prices. Is this yet another misperception? David Deming of the National Center for Policy Analysis writes 1, “the history of the petroleum industry is punctuated by periodic claims that the supply will be exhausted, followed by the discovery of new oil fields and the development of technologies for recovering additional supplies.” Even if no new oil supplies were discovered beyond those known today, Deming calculates based on projected growth in petroleum demand that supplies would not be exhausted until 2056. But he reviews historical data that show how “estimates of the world’s oil endowment have increased faster than oil has been taken from the ground,” concluding that the earth has enough petroleum resources to last at least until the year 2100. However, not all experts agree with Deming and, of course, nobody denies that petroleum is a non-renewable resource, in finite supply. But some people believe that long before humanity needs to worry about running out of oil, people will have devised better and more efficient energy technologies, including more renewable energy sources. 1.

Deming, David, Are We Running Out of Oil?, NCPA Policy Backgrounder

#159, January 28, 2003.

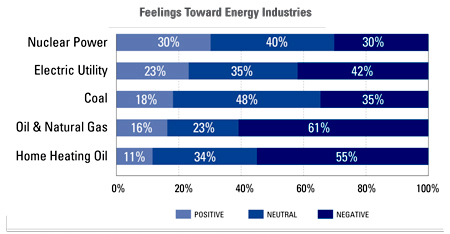

One of the “big picture” stories to emerge from our research is that US consumers lack confidence in nearly every part of the energy industry. That lack of confidence may be driven by the misperceptions already discussed, by media coverage, and by price fluctuations that hit consumers in the pocketbook. Let’s look at some of the specific areas where the American people lack confidence… In Energy Industries While the five major energy industries all appear very different, there is one thing they all have in common. As the following graph shows, most evoke more negative than positive feelings.

How positive or negative do you feel about each of the following industries?

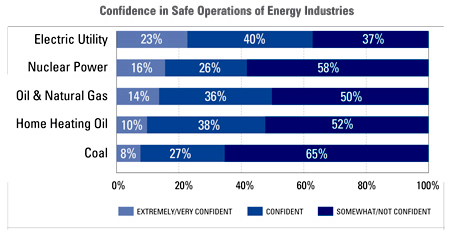

Based on everything you have read, seen or heard, how confident are you in the safe operations of the following industries?

In Energy Safety We also examined how each of these industries appears to the public in terms of safety issues. With the recent tragedies in the coal mines of West Virginia, it is not surprising to find that almost two-thirds (65%) of adults are somewhat or not at all confident in the safe operation of the coal industry, with only 27 percent saying they are confident and eight percent saying they are very or extremely confident. However, safety concerns are focused on other industries as well. The sector that seems to do the best in relation to safety is the electric utility industry. Nearly one in four (23%) are “extremely” or “very” confident in their safe operations, 40 percent are right in the middle, saying they are “confident,” while 37 percent are somewhat or not at all confident. While these differences are instructive, the overall conclusion is that the American public does not place a great deal of confidence in the safety of any energy industry. In Energy Supply Resilience After Natural Disasters In light of last year’s hurricanes, Katrina, Rita, Wilma and others, we also asked US adults how confident they are that these industries would be able to restore services after a natural disaster. Majorities have low or no confidence in all five industries. Electric utilities, however, may be again viewed as the “lesser of five evils,” with a somewhat lower (55%) rating of “somewhat/ not at all confident” than the coal (58%), nuclear (60%), home heating oil (60%) and the oil and natural gas (62%) industries.

How

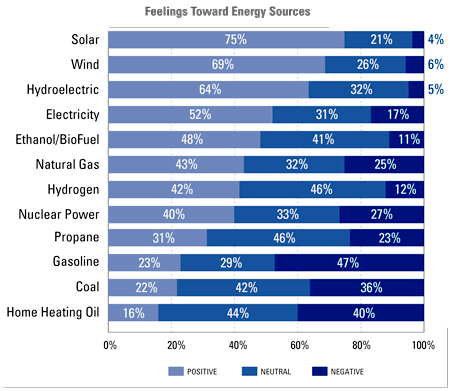

would you rate your feelings about the following types of energy sources? In Energy Sources Attitudes toward the 13 most prevalent energy sources vary greatly. They divide into three main categories. First, there are five energy sources toward which about half or more of the adult public feel positively. They are: solar, wind power, hydroelectric power, electricity, and ethanol/bio-fuel. The second group is made up of energy sources in the middle of the feeling scale where people may not have strong positive feelings toward them, but they also do not have strong negative feelings. This group includes natural gas, hydrogen, nuclear power, and propane. Among this group, hydrogen and propane tend to be viewed more with neutral feelings than with negativity; almost half (46%) are ambivalent, probably because they know very little about these two alternative fuels.

Nearly

half (47%) of Americans have a negative feeling toward

The final group is comprised of energy sources which have the least support among the American public, which also happen to be sources on which the United States is most heavily dependent. About one in four (23%) Americans have a positive feeling toward gasoline, while almost half (47%) have a negative feeling. Coal follows closely in terms of positive feelings (22%), but has fewer negatives as just over one-third (36%) of adults say they have a negative feeling toward coal. Finally, home heating oil receives the lowest positive rating at 16 percent with four out of 10 (40%) having a negative attitude toward this energy source. There’s a sort of love/hate relationship going on. While these ratings imply that Americans can’t live with these fuels, they clearly can’t live without them. It is interesting that electricity finds itself in the company of the highly rated safe/clean/renewable sources (solar, wind, hydro and ethanol), given that 70 percent of US electricity is generated by burning coal, oil or natural gas, and another 20 percent comes from nuclear power plants. Given their negative views toward these latter sources, it seems that most Americans are not aware, or they don’t stop to think, where electricity comes from. This points to yet another gap in public knowledge and understanding of energy issues.

Thinking

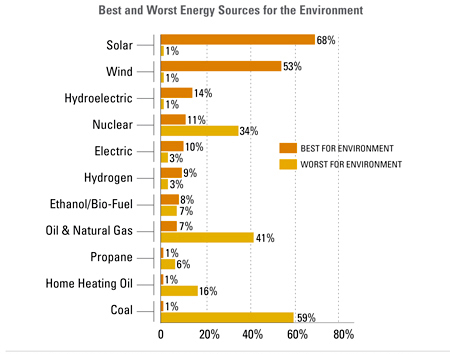

about the following energy sources, what two sources do Battleground Alaska Most of the negative or positive feelings toward different energy sources can probably be attributed to their perceived environmental impact. Only two energy sources, solar and wind power, are named by a majority of respondents as “best for the environment,” while coal is cited by a majority as one of the worst, followed by oil and natural gas. It is noteworthy that in a nation where 85 percent of energy comes from conventional fossil fuels (oil, coal and natural gas), most people are highly critical of these same sources on the grounds of environmental concern. Nothing illustrates this incongruity more dramatically than the debate over the Arctic National Wildlife Refuge (ANWR). For the past decade, and most sharply over the last two years, there has been an intense debate over whether to open up this large tract of land in Alaska to allow for the drilling of oil, or whether to preserve it as a wildlife refuge. Almost three-quarters (72%) of American adults say they have heard about the ANWR debate. Among these, we see an equal split between support for oil drilling (45%) and opposition to it (45%), with the other 10 percent saying they are not sure. This national rift has a number of dimensions:

The most relevant argument for opening ANWR to energy development is to lessen America’s dependence on foreign oil. This dependence is very real, of course, but it is not as great as most Americans think. According to our survey, half (51%) of US adults believe that more than two-thirds of the oil used in the United States is imported. In fact, the actual figure is close to 55 percent.

For decades, Americans and their leaders have talked about the need to replace conventional energy with renewable sources of energy. This is not a new phenomenon; when oil prices rise to record levels, calls for renewable energy sources grow stronger. It happened in the mid 1970s and the early 1980s. Only a few months ago, President George Bush made it a major focus of his State of the Union address. It is clear from our research that Americans share the dream of lessening dependence on foreign oil, and on fossil fuels in general, as reflected in their attitudes toward a variety of energy sources. Four of the five most positively rated energy sources are renewables (see "Feelings Toward Energy Sources" chart on above). Three-quarters of the adult public (75%) have a positive attitude toward solar energy, 69 percent feel positively about wind power, 64 percent feel good about hydroelectric power, and 48 percent feel positively about ethanol/biofuel, which is made from either corn or sugar cane.

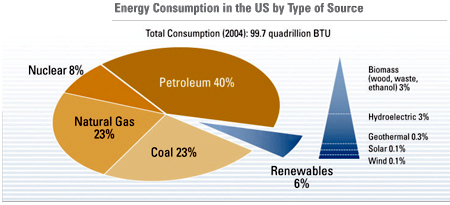

Source: U.S. Energy Information Agency As the chart above shows, these and other renewable sources currently account for only a very small percentage of America’s energy consumption (6%). Several administrations, including the most recent call to action by President Bush, have set up investment incentives in hopes of jump starting the technology improvements needed to make renewable fuels more economically viable. For example:

Partly as a result of government subsidies, there has been progress. Wind power has been in the news a lot lately. Other, less visible advancements include an increase in the number of government vehicle fleets powered by bio-diesel (a renewable fuel manufactured from vegetable oils and animal fats), and long-term research on hydrogen as a vehicle fuel. Ethanol shows some promise. Over five million of the 133 million cars on the road today are FlexFuel vehicles (FFVs) capable of running on E85 (85% ethanol, 15% gasoline). General Motors recently launched a high-profile FFV marketing campaign called “Live Green, Go Yellow,” and Chrysler announced last week that it will begin selling two flex fuel Jeeps this fall. But the limited availability of E85 – only about 600 service stations (out of about 169,000) in the United States currently sell E85 fuel – means most of these cars are still running on gasoline. While availability is expected to grow, clearly it is just a beginning. Development of renewable energy technologies is more intense now than it has ever been. But it will probably be a long time before renewable sources make a significant dent in the overall US energy picture. In the meantime, Americans will continue to rely on traditional energy sources to fuel their everyday lives.

Of all the industries and energy sources, the one that seems to inspire the greatest confusion is nuclear power. Negative attitudes toward the nuclear industry peaked after the 1979 accident at Three Mile Island and the hit movie The China Syndrome that same year. However, public perceptions about nuclear energy have clearly evolved over the past 25 years. As an industry, nuclear energy inspires positive attitudes among only 30 percent of the adult public, yet that is the highest positive rating of all the industries measured. As an energy source, four out of 10 have positive feelings toward nuclear; while that is not at the top, it is also not at the bottom of the scale. Concerning nuclear energy’s impact on the environment, attitudes are polarized. While one-third (34%) say it is one of the worst for the environment (behind coal and oil and natural gas), it is also rated fourth best for the environment. The area where people appear to have the greatest concern is over safety issues, as more than half (58%) are somewhat or not at all confident in the safety of the nuclear industry. Only the coal industry is rated worse. Men are more likely than women to be highly confident (28% very or extremely confident vs. 5%, respectively). On the flip side, 70 percent of women say they are somewhat or not at all confident in the safety of the nuclear industry’s operation as compared to under half (45%) of men who have that same attitude. It’s interesting to note that no nuclear workers or members of the public have ever died as a result of exposure to radiation due to a commercial nuclear reactor incident in the United States, including Three Mile Island. But the possibility is apparently never far from many people’s minds.

Currently, there are 104 operational nuclear power plants in the United States, which provide 20 percent of the total electricity generated in the country. However, the nation’s nuclear generating infrastructure is aging. The last time a new nuclear reactor came on line was in 1996. With demand for electricity in the United States projected to increase 40 percent by the year 2025, and in light of the clean air benefits of nuclear when compared with gas-fired and coal-fired electrical generation, there is growing bipartisan support in Washington for taking a new look at nuclear power. Recent developments suggest that the time for the construction of new nuclear power plants may come sooner than later:

Given the dynamics of this high profile issue, we can expect public attitudes about nuclear power to remain divided for some time to come.

1. Energy Will Remain Top Concern. So long as energy prices remain high (or “unreasonably high” in the eye of the consumer) most major energy industries, will be in the public spotlight. In part, the consumer’s view seems to be based on misinformation, as most people overestimate the contribution of corporate profits to prices. Another problem, for the oil industry especially, is American distrust of big companies generally (not just “big oil” but “big government”, “big business” and, most recently, “big pharma”). That will be difficult to change, even if good arguments can be made as to why energy companies need to be big. The data suggest that while it would be very difficult for energy companies to become less unpopular unless prices come down, (or, possibly, are stable so people get used to them) there are some areas where, as we have shown, the energy industry is hurt by misperceptions which might be changed (albeit not easily). What is clear is that many Americans have a love/hate relationship with energy. They love to consume it and want access to inexpensive gasoline, oil, natural gas, electricity and other energy sources. On the other hand, they react angrily to higher prices and to big companies. They favor energy conservation, and are deeply suspicious of new drilling that might endanger the environment. However, they react strongly against proposals for higher energy taxes that would encourage conservation. Additionally, they tend to favor government legislation to mandate higher gas mileage. In other words most people are human, if not rational. They want the gain without the pain. 2. The Popularity of Alternative, Renewable Energy Sources. The contrast between the positive public attitudes to solar, wind and hydro energy on the one hand and the negative attitudes to oil and coal on the other is very striking. To the extent that they can, energy companies which are seen to be advocates for, and investors in, popular energy sources are likely to benefit. It is interesting that foreign-owned oil companies (BP and to a lesser extent Shell) adopted this strategy earlier, and with much greater enthusiasm, than American-owned companies.

Nuclear energy, as an energy source, is more popular than propane, gasoline, coal or home heating oil. 3. Nuclear Power. Most people are still concerned about the safety of nuclear power (even if they are more concerned, currently, about the safety of the coal industry). However, people now are less likely to feel negatively toward the nuclear power industry than toward other energy industries. And, as an energy source, nuclear energy is more popular than propane, gasoline, coal or home heating oil. Two important things have happened since The Three Mile Island accident put a stop to nearly all nuclear power plant construction. One is the “dog that didn’t bark.” While Chernobyl was a very big deal, the absence of any significant nuclear accidents in the United States has probably had some effect. However, the big new issue is global warming. The polls have shown that most people see global warming as a big concern, and that they believe man-made greenhouse gases are a major contributor. The greater these concerns become, the stronger the arguments for nuclear power become. Energy is among the top issues affecting our day-to-day lives in direct and sometimes dramatic ways. It’s also one of the more complicated, shaped by global economic forces, political agendas, consumer behavior, changing technology—even the weather. Clearly, the public does not always understand or appreciate that complexity. People just want the light to turn on, the house to stay warm, and the car to accelerate when they step on the gas pedal. As energy-related companies deal with consumers, and as policy makers reach out to voters, they should keep in mind the need to educate as well as persuade.

The Harris Poll® was conducted online within the United States between January 12 and 17, 2006 among 1,467 adults (aged 18 and over). Figures for age, sex, race, education, region and household income were weighted where necessary to bring them into line with their actual proportions in the population. Propensity score weighting was also used to adjust for respondents’ propensity to be online. In theory, with probability samples of this size, one could say with 95 percent certainty that the overall results have a sampling error of plus or minus 3 percentage points of what they would be if the entire US adult population had been polled with complete accuracy. Sampling error for subsamples such as age, gender, and political party ID breakouts is higher and varies. Unfortunately, there are several other possible sources of error in all polls or surveys that are probably more serious than theoretical calculations of sampling error. They include refusals to be interviewed (nonresponse), question wording and question order, and weighting. It is impossible to quantify the errors that may result from these factors. This online sample was not a probability sample. Note: Percentages may not add up to exactly 100% due to rounding. These statements conform to the principles of disclosure of the National Council on Public Polls.

Harris Interactive Inc. (www.harrisinteractive. com), based in Rochester, New York, is the 13th largest and the fastest growing market research firm in the world, widely known for The Harris Poll® and for its pioneering leadership in the online market research industry. In an increasingly chaotic and competitive world, Harris Interactive provides researchdriven insights and strategic advice to help clients make more confident decisions that strengthen the bonds between their enterprise and its key stakeholders, leading to measurable and enduring improvements in performance. Harris Interactive is proud to have been recognized for the value of its work on seven David Ogilvy Award-winning campaigns. Harris Interactive serves clients worldwide through its offices in the United States, Europe, and Asia, its wholly-owned subsidiary Novatris in Paris, France (www.novatris.com), and through an independent global network of affiliate market research companies. by Jean Statler The Harris

Report, Volume I, Issue I, May 2006

© 2015 TLC Magazine Online, Inc. |