Real Social Security Reform

Small Business Encourages Market Based Reform

SMALL BUSINESS WATCHES SOCIAL SECURITY REFORM WORK FOR PERSONAL RETIREMENT ACCOUNTS

The

National Federation of Independent Business

Small-business

owners, like all Americans, are concerned about the future of Social

Security. Their perspective on the issue is unique, as it is both that

of the future retiree and of the employer paying the payroll taxes.

The problem for small business

-

According

to Social Security trustees, if nothing is done to fix the problem

with Social Security, the program is expected to become insolvent

by 2052.

-

Over

the next 50 years, the number of workers available to support each

Social Security beneficiary will drop from a rate of 3.4 to 1 to

only 2.1 to 1. The cost of supporting the current system will increase

69 percent during that period. (Strengthening Social Security

and Creating Personal Wealth for All Americans, Report of the President’s

Commission, December 2001, p.34)

-

According

to the Congressional Budget Office, approximately 80 percent

of Americans pay more in payroll taxes than in federal income taxes. (Congressional Budget Office, Economic Stimulus: Evaluating

Proposed Changes in Tax Policy, January 2002, p.12, footnote 7)

-

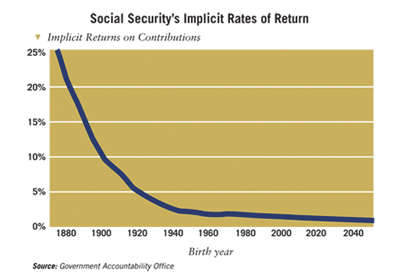

A

25-year-old male with an average income is predicted to receive

a –0.82 percent rate of return on his Social Security taxes.

In other words, he will pay more into the system in taxes than he

will receive back in benefits. (How to Fix Social Security,

by David C. John, The Heritage Foundation, Nov. 17, 2004)

NFIB advocates four principles to ensure Social Security reform

is fair to small business:

-

Individually

controlled Personal Retirement Accounts should be a major part of

any Social Security reform. An NFIB member ballot question in 2005

found that 71 percent of members believe that Social Security should

be reformed to allow individuals to invest in PRAs.

-

Payroll

taxes must not be increased. Small business owners not only pay

their own Social Security payroll taxes, they also contribute taxes

on behalf of their employees. Reform will cost money; however, NFIB

members oppose increasing payroll taxes as afinancing option.

-

Social

Security reform should not increase paperwork burdens on employers.

A principal small-business concern about Social Security is administrative

complexity. Reform plans must take steps to ensure that paperwork

burdens on employers are not increased.

-

Social

Security should continue its commitment to provide benefits to retired

workers. Eighty-five percent of NFIB members believe that even with

private accounts, the program should remain mandatory and that retirees

should receive a minimum benefit.

© 2015 TLC Magazine Online, Inc. |