|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

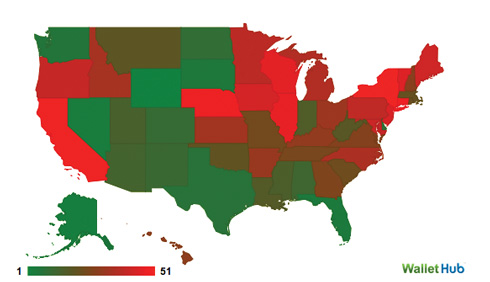

| Rank | State | Avg. Annual State & Local Taxes | % Difference from National Avg. | Adj. Rank (based on Cost of Living Index) |

| 1 | Wyoming | $2365 | -66% | 1 |

| 2 | Alaska | $2791 |

-66% | 4 |

| 3 | Nevada | $3370 | -52% | 2 |

| 4 | Florida | $3648 | -48% | 3 |

| 5 | South Dakota | $3766 | -46% | 5 |

| 6 | Washington |

$3823 | -45% | 6 |

| 7 | Texas |

$5193 | -25% | 7 |

| 8 | Delaware | $5195 | -25% | 12 |

| 9 | North Dakota | $5588 | -20% | 13 |

| 10 | Colorado | $5674 | -19% | 14 |

| 11 | New Mexico |

$5822 | -16% | 8 |

| 12 | Alabama | $5846 |

-16% | 9 |

| 13 |

Arizona |

$6057 | -13% | 17 |

| 14 | Utah | $6098 | -13% | 11 |

| 15 |

Mississippi |

$6210 | -11% | 10 |

| 16 | Indiana | $6358 | -9% | 15 |

| 17 | Louisiana |

$6564 |

-6% | 18 |

| 18 | West Virginia | $6598 | -5% | 19 |

| 19 | Montana | $6641 | -5% |

20 |

| 20 | Oklahoma | $6795 | -2% |

16 |

| 21 | Massachusetts | $6884 | -1% | 35 |

| 22 | Rhode Island | $6905 | -1% | 40 |

| 23 | South Carolina | $7070 | 1% | 24 |

| 24 | Missouri | $7220 | 4% | 22 |

| 25 | Tennessee | $7252 | 4% | 21 |

| 26 | Georgia | $7319 | 5% | 25 |

| 27 | Virginia | $7333 | 5% | 29 |

| 28 | New Hampshire | $7419 | 6% | 41 |

| 29 | Hawaii | $7427 | 7% | 48 |

| 30 | Kentucky | $7472 | 7% | 23 |

| 31 | Arkansas | $7557 | 8% | 26 |

| 32 | Ohio | $7604 | 9% | 28 |

| 33 | Kansas | $7695 | 10% | 30 |

| 34 | Idaho | $7776 | 12% | 27 |

| 35 | North Carolina | $7789 | 12% | 32 |

| 36 | Michigan | $7867 | 13% | 31 |

| 37 | District of Columbia | $8034 | 15% | 46 |

| 38 | Minnesota | $8261 | 19% | 36 |

| 39 | Pennsylvania | $8344 | 20% | 34 |

| 40 | Oregon | $8416 | 21% | 42 |

| 41 | Maryland | $8571 | 23% | 44 |

| 42 | Maine | $8622 | 24% | 43 |

| 43 | Iowa |

$8788 | 26% | 33 |

| 44 | New Jersey | $8830 | 27% | 47 |

| 45 | Vermont | $8838 | 27% | 45 |

| 46 | Wisconsin | $8975 | 29% | 39 |

| 47 | Illinois | $9006 | 29% | 38 |

| 48 | Connecticut | $9099 | 31% | 49 |

| 49 | Nebraska | $9450 | 36% | 37 |

| 50 | California | $9509 | 36% | 50 |

| 51 | New York | $9718 | 39% | 51 |

|

Lowest Real Estate Tax Rates |

|

No Income Taxes (State & Local) |

|

Lowest Vehicle Sales Taxes |

|

Lowest Sales Tax Rates (State & Local) |

|

Lowest Fuel Taxes (per gallon) |

|

Lowest Alcohol Taxes (per capita per yr) |

FOOD TAX RATES

|

Worst States |

VS |

35 States with No Tax on Food

|

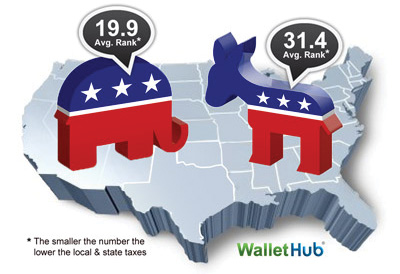

RED STATES IMPOSE LOWER TAXES THAN BLUE STATES

Now that tax season is over and the learning experience is renewed once again, the following tax advice will be, perhaps, more meaningful providing insights that may be helpful as you prepare for 2015. - Editor

Ask the Experts: Best Tax Advice

Mistakes are common come tax season. They’re expensive too. So, in order to help people avoid costly tax prep errors we asked tax experts from around the country what the most common mistakes are as well as how we can correct them. You can check out their responses below.

|

“One mistake is not paying attention to all that is on your tax return and related documents. Many people just look at the line that says amount owed or refund thinking that is their federal tax liability. They should look at the total tax line of their Form 1040 (line 61) to see their total tax. They should also look at their W-2 wage forms to see what additional taxes they paid for FICA and Medicare (boxes 4 and 6). The FICA and Medicare tax was matched by the employer, but in effect paid by the worker in the form of lower wages. Take all of these federal income and payroll taxes and divide it by your taxable income to find your average tax rate. We often hear news stories about people with less than $50,000 of income not paying any tax. That usually is not true. Many of these individuals are wage earners and have at least paid payroll taxes of 15.3% (employee and employer share). |

Also, individuals pay federal excise taxes when they buy gasoline, alcohol, tobacco, airline tickets and a few other items. And, don't forget to look at what your state income and other state and local taxes are to get the full picture of what you contribute to funding government operations.”

- Annette Nellen, San Jose State University

|

“One of the biggest mistakes taxpayers make when having their returns prepared by a paid tax return preparer is not to look over and understand what has - Caroline Tso Chen, Santa Clara University School of Law |

|

“One of the most common reasons why people overpay on their investment related taxes is by failing to maximize the use of any capital losses they may have. Generally, if you have sold an investment at a loss, you should try to sell an appreciated investment at a gain so you can benefit from the loss this year. However, be sure to anticipate your tax rate in the following year because in some circumstances it might be better to defer taking your losses. People also overpay on their investment related taxes by unintentionally purchasing stock, selling it, and then repurchasing it 30 days after the sale. This causes the ‘wash sale’ rules to apply which generally denies the taxpayer from claiming the loss. This issue also arises if the taxpayer purchases substantially identical stock 30 days before the date of the sale of the stock that he or she holds.” - Orly Mazur, SMU Dedman School of Law |

|

“There are several common mistakes that result in the overpayment of investment related tax that come up with some regularity. The first is that money is not invested in a tax deferred investment like an IRA or a 401k account so it doesn't grow tax free. Related to these types of investments is another common mistake and that is the situation where, even though money is initially invested in these types of accounts, that money is withdrawn prior to age 59 1/2. When that happens, not only is ordinary income tax due on the withdrawal, but taxpayers end up paying a 10% penalty tax for the early withdrawal. A third common reason for overpayment of tax is that investors often buy taxable investments when tax free investments like municipal bonds might result in a better rate of return once taxes are factored into the calculations. |

A final common mistake that is often made is that capital assets are sold prior to the one year holding period that entitles investors to reduced rates of tax.”

- David J Kautter, American University

|

“Individuals should understand the differences between ‘above the line’ and ‘below the line’ deductions. Above the line deductions are more advantageous because they reduce taxable income, the tax calculation base, while below the line deductions allow taxpayers to realize a savings based on their marginal tax rate. In addition, many individuals do not realize that certain items touted as deductions (charitable contributions) are in fact only deductible if the taxpayer is eligible to itemize on his/her return.” - Maureen J. Bruns, Carl H. Lindner College of Business, University of Cincinnati |