|

||

|

Elizabeth Stribling & Kirk Henckels |

Greetings,

Participating in the market for luxury properties demands extraordinary intelligence, diligence and discretion. Especially in New York City. Especially for properties valued in excess of $5 million.

In this rarefied market every sale is unique. Market solutions must be customized. Confidentiality is imperative. Specifics such as addresses, pricing and ownership must be carefully protected.

In this report Stribling invites you to review the highlights of the year 2007 and the current status of the natal 2008 market. While this report has been thoughtfully prepared and our data base is second to none, we remind both buyers and sellers that the figures reported are to be used only as a guide to reflect market trends.

Elizabeth F. Stribling, President

Stribling & Associates

OVERVIEW OF THE 2007 LUXURY MARKET

It is a remarkably precarious time to be writing an analysis of the Manhattan luxury real estate market. Rarely has there been such a clear cut division between “that was then and this is now” in terms of the economy going into 2008. However, despite the sturm und drang of the last quarter of 2007 and the extreme current turmoil in the financial markets, the luxury real estate market over $5m continued to break records throughout 2007, even in the last quarter, and it has continued to do so into 2008. Granted the dollar volume was off for cooperatives in 2007, but only because of very limited inventory at the top of the market, which had declined by as much as 30% over 2006. The townhouse numbers in 2007 increased only slightly over 2006 while the condominium numbers broke all records. Indeed, the condominium market seemed to explode in 2007 as both The Plaza Hotel and 15 Central Park West started closing on their condominium units at record prices. Some reports indicate that these two projects were mostly responsible for the approximately 18% increase in the average price for condominiums in 2007.

As predicted in our Mid Year Report, the strong momentum of luxury real estate sales continued unabated throughout the second half of 2007 despite the subprime problems. It was a clear example of continued strong demand, even more money and no supply. Miraculously, and despite it all, this pattern continues into 2008.

COOPERATIVES

After a huge, 40.4% growth in 2006, the 2007 luxury cooperative market over $5m was strangled by a lack of inventory. While remaining over the $1 billion mark, total volume of cooperative sale fell 6.5% to $1,286,683,310 in 2007 from $1,376,452,286 in 2006. Likewise, the number of sold units fell 17.4% to 128 in 2007 from 155 in 2006. The increased strength at the high end is evidenced by the 13.2% increase in the average price of cooperatives over $5m, which rose to $10,052,213 in 2007 versus $8,880,337 in 2006. This is easily explained by the 26.9% increase to 33 in 2007 from 26 in 2006 of cooperative sales with prices ranging from $10m to $20m.

As one would expect in an inventory-starved market, the spread between ask and sales price narrowed to 2.2% in 2007 from an already low figure of 3.4% in 2006. Likewise, the percentage of deals at or above the asking price rose to 39.4% in 2007 from 35.5% in 2006.

There have been many highly publicized sales in 2007. Ironically, the highest cooperative sale in 2007 was also the highest sale in 2006. David Geffen paid $31.5m in 2006 for a duplex penthouse at 810 Fifth Avenue, which had once been the apartment of Nelson Rockefeller. Mr. Geffen then decided to sell the apartment in 2007 for $37.5m directly to Peter Peterson, co-founder of the Blackstone Group. That is a 19% return in just over a year.

It is worth noting that the number of cooperative sales over $20m remained level at eleven, however this is very misleading and not indicative of the true strength of the high-end market in the last half of 2007, even after the subprime debacle. The truth lies in those closings that have already occurred in 2008 and those that are currently pending in 2008, all of which were signed in 2007. There have already been four closings over $20m in 2008. The highest of these is a record-breaking $46m for an uncombined duplex penthouse at 1060 Fifth Avenue. Another closed sale was for a reported $33m for Vera Wang’s 778 Park Avenue cooperative. Interestingly, this purchase and another pending purchase at 740 Park Avenue are being made by Ira Rennert for his two married daughters.

Even more persuasive than the four 2008 closings over $20m are the nine sales over $20m in contract waiting to close, ranging up to $35m for a large apartment at the Stanhope development on Fifth Avenue. These $20m+ deals, if they all do close, would total thirteen deals over $20m in the first half of 2008, already more than the eleven such deals done in all of 2007.

Of the nine pending sales over $20m, three are on Fifth Avenue, three are on Park Avenue, two on Central Park West and one on the East River in the 50’s. All are in architecturally-important prewar buildings.

This is all very impressive. And even more so because these aforementioned statistics include only one pending closing of the cooperative development of The Stanhope at 995 Fifth Avenue and none at 110 Central Park South. Both of these developments are unusual in that they are cooperatives due to the fact that they are built on leased land and, therefore, are not legally allowed to be condominiums. Unlike the condominium market, the cooperative market doesn’t usually have large developments whose closings suddenly skew all the numbers as in the case of The Plaza and 15 Central Park West.

Given the strong number of pending sales, the first half of 2008 should break all records, and not just in the $20m and up segment. Currently, there are 79 cooperatives over $5m with pending closings versus 49 last year. These 79 pending sales are already more sales than were reported in the first half of 2007. Inventory continues to be very low, demand strong and, regardless of the stock market, there is still a great deal of wealth in the market. The first half of 2008 seems to have already guaranteed its statistical performance even though it has barely begun. It is the second half of 2008 that causes concern.

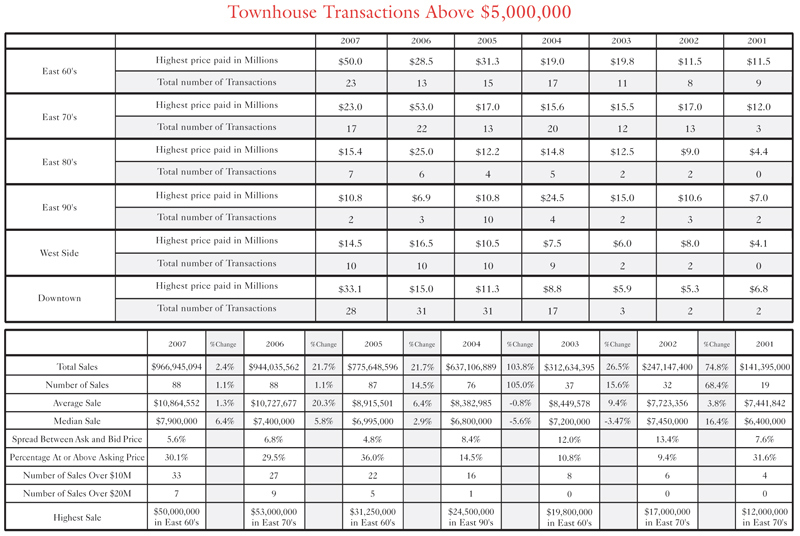

TOWNHOUSES

In 2007, the $5m and up townhouse market performed in a manner remarkably similar to that of 2006. While the inventory level of quality properties was quite low, it was sufficient to support a slight increase in volume. The total sales of family townhouses increased 2.4% to $966,945,094 in 2007 from $944,035,562 in 2006. The number of sales remained basically unchanged, increasing 1.1% to 89 in 2007 from 88 in 2006. The most significant change is in the median sales which increased 8.1% to $8,000,000 in 2007 from $7,400,000 in 2006, once again underlying the strength at the higher end of the market.

As one would expect in a market with limited inventory, the spread between asking price and selling price decreased to 5.6% in 2007 from 6.8% in 2006. Surprisingly, the percentage of properties selling at, or above asking price increased only slightly to 30.1% in 2007 from 29.5% in 2006.

While not breaking the $53m record sale of the Harkness House at 4 East 75th Street in 2006, the highest townhouse sale in 2007 was $50m for 15 East 64th Street, a 31-foot wide, beautifully renovated townhouse owned by Edgar Bronfman, Jr. Mr. Bronfman sold the house, with its highly coveted 64th Street address, directly to Len Blavatnik, a friend who seemingly has at least two other very major residences in Manhattan. Ironically, the fourth largest sale, for $33.0m at 7 East 67th Street, was made by Mr. Bronfman’s brother, Matthew, also directly.

Townhouses downtown comprised 31.5% of houses sold over $5m in 2007 and a remarkable 41.1% of the currently pending sales in 2008. Also, the third largest townhouse sale, and a record for downtown, was the $33.1m sale of a 55-foot wide house at 11 West 10th Street.

Like cooperatives, there was particular growth in the $10m to $20m segment. In 2007, there were twenty-six sales in this category versus eighteen in 2006, an increase of 44.4%. However, the $20m and up category actually decreased slightly in number of sales to seven in 2007 versus nine in 2006. Currently, there has only been one 2008 closing over $20m. It is the $35m sale of a 25-foot wide townhouse at 36 East 75th Street, which was bought by the Russian Federation.

As we enter 2008, it is interesting to note that, unlike cooperatives, the strength of the pending townhouse sales is not at the high end, though several new $20m+ listings came on the market in the last half of 2007. Indeed, there is only one other sale over $20m pending in 2008. It is the potentially record-breaking 2008 sale of 777 Washington Street, a 20,000 square foot, beautifully renovated townhouse with private driveway, multiple terraces and 20 foot ceilings, asking $38.5m. The current strength in the townhouse market is under $20m, where there are thirty-three pending sales in 2008 versus twenty-seven in 2007.

Unlike cooperatives, the statistical performance of the townhouse sector for the first half of 2008 remains unclear, especially at the high end.

CONDOMINIUMS

(note bene: Due to the misleading nature of recording condominium ownership and the combining of units, this report does not attempt a statistical analysis of the condominium market.)

“Explosive” is the only appropriate word to describe the 2007 condominium market. It is the unique nature of this market that it experiences statistical swings as each large development project starts to close. In the case of 2007, there were multiple, large, super-luxury developments that came to closings. The most prominent of these is The Plaza, which with 181 residential condominium units and 152 hotel condominium units has a projected combined sellout of just under $2 billion. Not far behind is the development of 15 Central Park West. Both set new standards for luxury and both had sales over $6,000 per foot.

With this kind of stage set, there were many records broken. The Plaza had four sales over $50m and a recordbreaking $60m+ sale of 13,000 square feet to developer Harry Macklowe. At 15 Central Park West there were at least twenty-eight listings asking over $15m, topping out at about $46m, unless, of course, buyers wanted multiple units, as many did. It is believed that the highest sale there was for a $42.4m penthouse to ex-Citigroup CEO Sandy Weill and his wife.

Last year at this time, the big worry was whether the New York market could absorb the large number of new condominium developments coming on the market. Given this widely publicized concern, some developers put their projects on hold. However, the vast majority proceeded and most did so successfully. Once again, no one expected the market to remain so strong, especially after the subprime problems surfaced. While inventory has remained relatively level, the average price per square foot increased in 2007 versus 2006. Once again, it is necessary to caution that all the condominium numbers are skewed by The Plaza and 15 Central Park West.

While much attention has been drawn to the importance of the foreign buyers, it should be pointed out that the majority of the buyers at The Plaza were American and the majority of those were New Yorkers. Nonetheless, the foreign buyers have helped the absorption rate of the condominium market as American real estate looks increasingly cheap. With comparable properties in London selling at double the price per square foot, one almost wonders what took them so long.

DOWNTOWN

Downtown saw its trend continue towards full service condominiums with the near sell out of 40 Mercer Street, 40 Bond Street and 50 Gramercy Park North, among others. Among these three developments, they offered almost every amenity, from large swimming pool to garage, gymnasium, valet, concierge, hotel service, not to mention the highest levels of technology available. As a result, the other trend continues of uptown empty nesters opting for a new and different lifestyle downtown They have just been waiting for the services to be offered.

One might expect the loft market to suffer from the onslaught of full service condominiums being built downtown, but this would appear not to be the case. The average price per square foot for a loft is up significantly in 2007 over 2006 and is even higher than the average price per square foot for an Upper East Side cooperative.

While downtown exceeds uptown in many segments of the middle market, this has not been the case for the high end of the market. Yet, the trend towards parity of uptown and downtown in high-end sales strengthens every year. Witness the aformentioned record breaking downtown sale of $33.1m for a townhouse on West 10th Street in 2007 and the pending sale of the townhouse at 777 Washington Street with an asking price of $38.5m. Also, the reported pending sale of a condominium at One Madison Park for $31m, a record below 57th Street.