Everyone knows that auto insurance is mandatory except in New Hampshire. Furthermore, we know that our credit scores dictate the types of loans and credit cards for which we can garner approval. But when it comes to the connection between credit scores and car insurance, most of us are in the dark.

With that in mind, WalletHub set out to determine:

1) how transparent insurance companies are in disclosing the use of credit data in underwriting decisions;

2) how transparent they are about the source of their credit data; and

3) the extent to which credit data impacts insurance policies across the 50 states and the District of Columbia.

In evaluating the importance of credit data to insurance underwriting, WalletHub obtained quotes from five of the largest auto insurance providers in the country for two hypothetical consumers who are identical save for the fact that one has excellent credit while the other has no credit. This allowed us to isolate for the role of credit in insurance policy pricing.

It is important to note that the exact credit based pricing fluctuations discussed throughout the report may not hold true for all consumers given the multitude of other factors that contribute to the insurance policies each of us are extended. In other words, the fact that credit scores impact insurance premiums to a significant extent should be the main takeaway for consumers, rather than the exact amount of the impact.

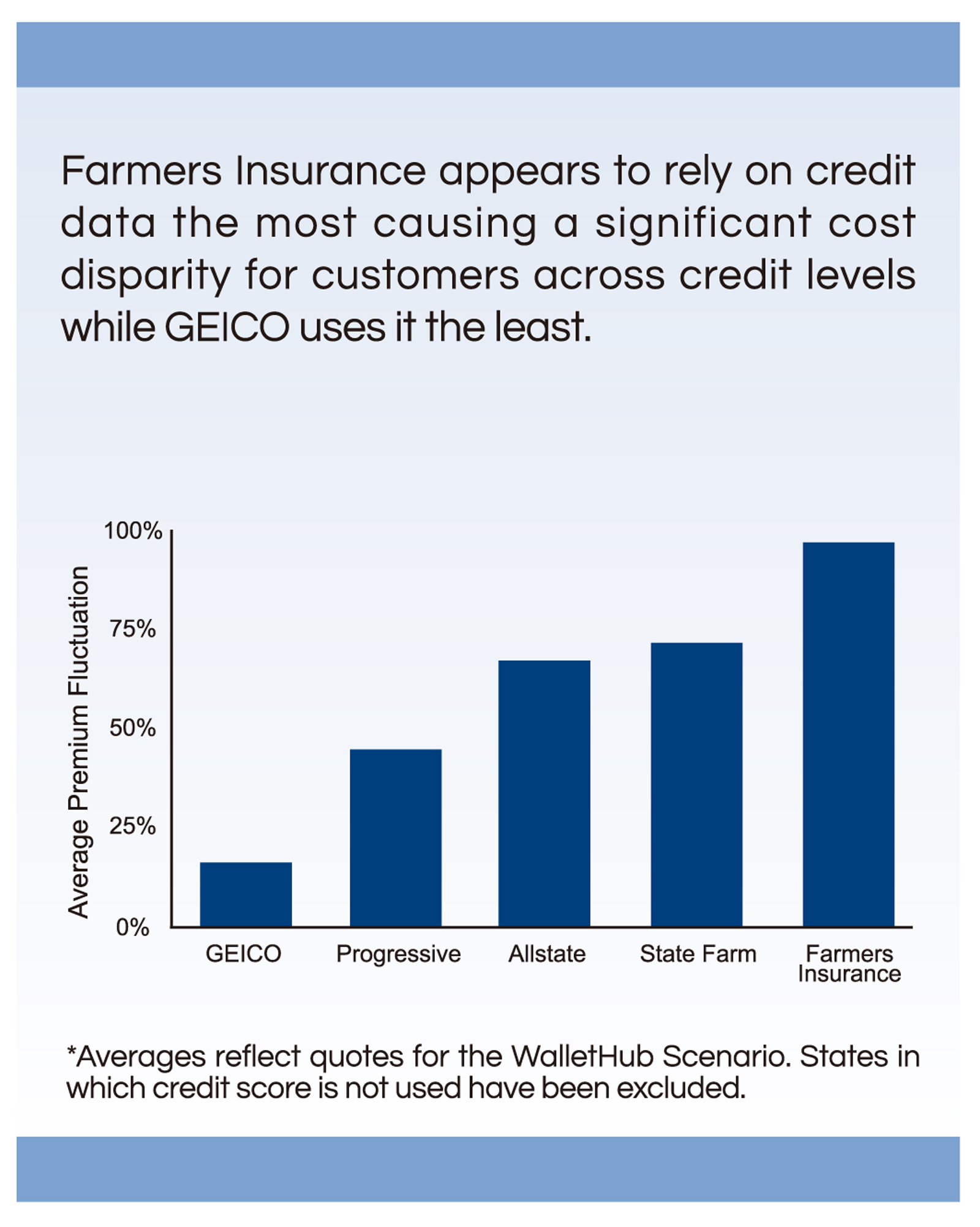

People with no credit pay an average of 53% more for car insurance than people with excellent credit with some states seeing fluctuations as high as 122%.

In order to determine the impact of consumer credit data on car insurance premiums, we collected premium quotes from the websites of five of the largest insurance providers in the United States based on the total number of insurance premiums issued, according to SNL Financial.

In light of the fact that insurers use numerous variables in pricing their policies, we obtained quotes for two hypothetical consumers, identical save only for their credit history. More specifically, one consumer has excellent credit while the other has no credit history.

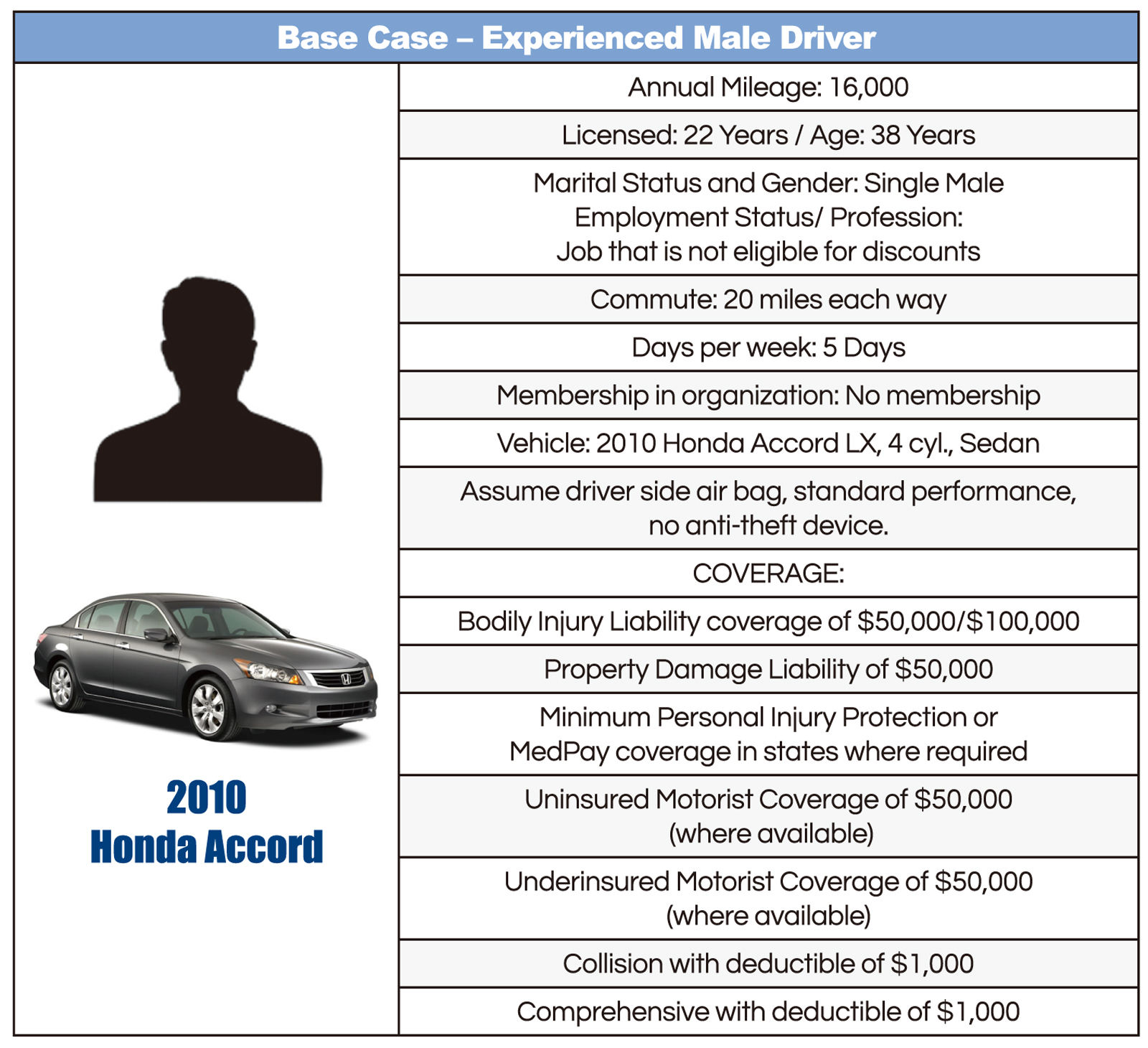

Our base case, also referred to as the "WalletHub Scenario" in this report, assumes the following details about the driver and the automobile:

The insurance coverage details were used as guidelines, as different states have different requirements. Where we were unable to match the coverage details to the above specifications, we chose the value closest to our base case data, or the cheapest option for the coverage limits that were available. State specific and other miscellaneous taxes have been included in the quote as needed.

In order to receive a quote from the insurance provider websites, a specific zip code was required. For each state in which the company was active, we chose zip codes where the average household income was closest to the average income for the state as a whole. Data was collected between May 17 - May 30, 2016.

Once we received the quote with the total amount of the premium, we divided the amount by the number of months the premium was for in order to get an equal monthly payment and a fair comparison point.

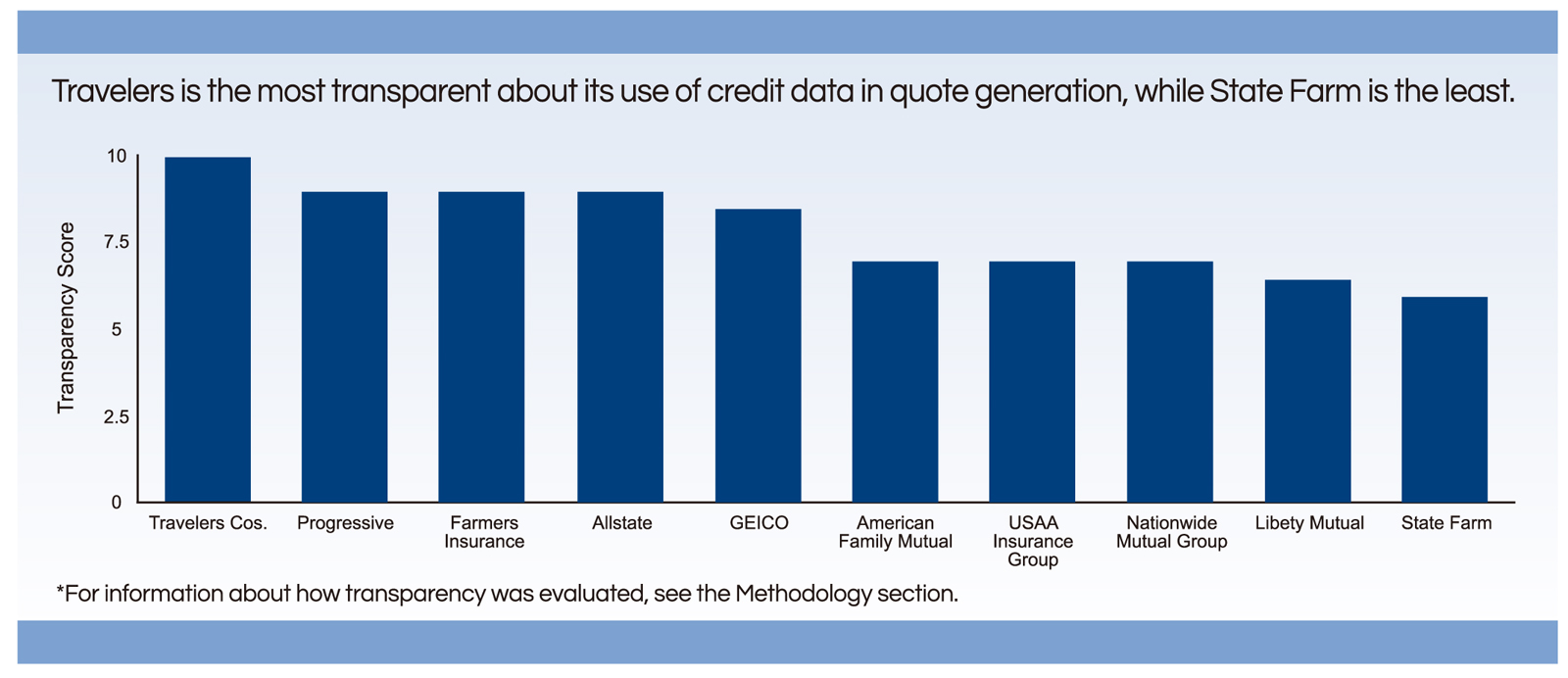

We also evaluated the top 10 insurance companies in the in order to determine how transparent each company is about the use of consumer credit information in their pricing policies. We reviewed each company's website based on the following criteria:

A. How easy is it for a consumer to find out if the insurance provider is accessing their credit information and using it to provide pricing information?

This question is worth 5 points total, and we scored it based on 2 dimensions: location of information and how prominent it is. If the information could not be located, no points were given.

Based on location:

1 point- If information is found on the first page of the quoting process.

0.5 points - If information is found on a subsequent page of the quoting process.

Based on how prominent the information is:

4 points - Prominent and normal size font.

3 points - Prominent and small size font.

2 points - Prominent accompanied by a pop-up/expanding section.

1 point- Not prominent.

B. How easy is it for a consumer to determine which credit reporting agency credit data is being requested from?

This question is worth 5 points total.

5 points - Information can be found on site and is a part of the quoting process.

4 points - Information can be found on the site, but needs to be searched for outside of the quoting process.

2 points - Information can be obtained through customer service lines.

1 point - Information is provided by the Public Relations department.

0 points - Information is not present on the website, cannot be obtained through customer lines or from the Public Relations department.

We sent the transparency scores to the included insurance companies so that they may verify the data and provide comments or corrections. All but GEICO and Progressive responded, and any necessary changes were made. We did not seek confirmation of premium fluctuation data, as the insurers' public relation departments previously informed us that such information is impossible to verify.