2019 | Adam McCann, Financial Writer

U.S. economic growth depends heavily on the performance of individual states. But some contribute more than others. California, for instance, blossomed in 2017 as the fifth largest economy in the world, boasting a GDP larger than that of countries like the U.K., France and India.

Meanwhile, Alaska, a state with valuable natural resources, is struggling with the highest unemployment rate in the country, at 6.5%.

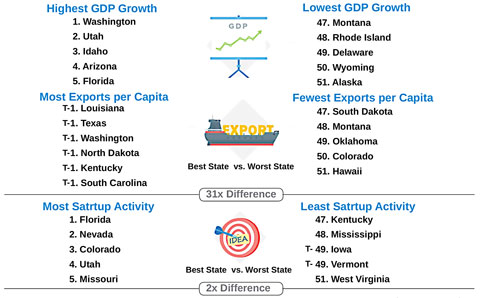

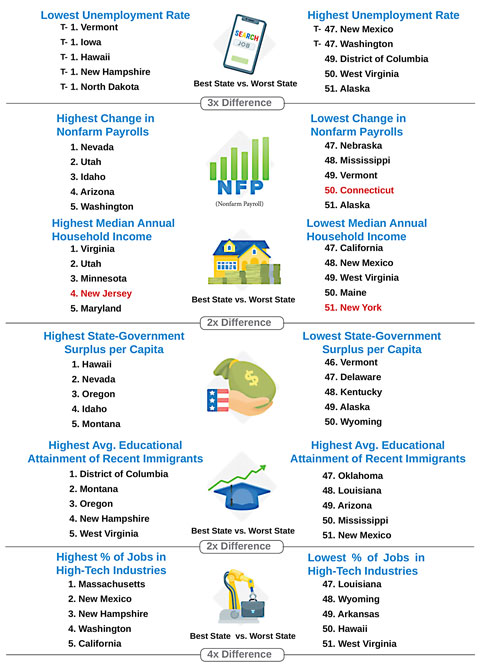

In order to determine which states are pulling the most weight, WalletHub compared the 50 states and the District of Columbia across 28 key indicators of economic performance and strength. Our data set ranges from GDP growth to startup activity to share of jobs in high tech industries.

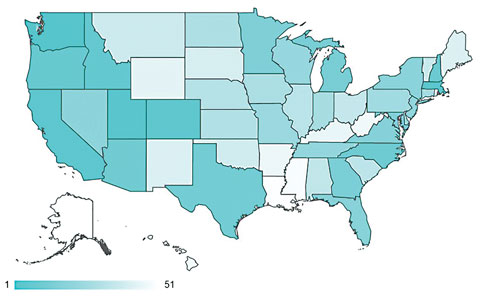

| Overall rank (1=Best) | State | Total Score | ’Economic Activity’ Rank | ’Economy Health’ Rank | ’Innovation Potential’ Rank |

|---|---|---|---|---|---|

| 1 | Washington | 77.60 | 1 | 4 | 2 |

| 2 | Utah | 73.51 | 2 | 1 | 10 |

| 3 | Massachusetts | 70.23 | 5 | 20 | 1 |

| 4 | California | 69.13 | 3 | 35 | 3 |

| 5 | Colorado | 63.79 | 9 | 3 | 8 |

| 6 | District of Columbia | 58.97 | 4 | 15 | 15 |

| 7 | Idaho | 58.23 | 13 | 2 | 18 |

| 8 | Oregon | 56.83 | 16 | 22 | 7 |

| 9 | New Hampshire | 56.75 | 20 | 17 | 5 |

| 10 | North Carolina | 55.90 | 15 | 11 | 12 |

| 11 | Arizona | 55.54 | 12 | 10 | 14 |

| 12 | Texas | 55.17 | 10 | 7 | 20 |

| 13 | Michigan | 53.87 | 22 | 31 | 4 |

| 14 | Georgia | 53.27 | 6 | 18 | 26 |

| 15 | Minnesota | 51.84 | 28 | 16 | 11 |

| 16 | Maryland | 51.71 | 18 | 37 | 9 |

| 17 | Virginia | 51.33 | 14 | 13 | 25 |

| 18 | Florida | 50.74 | 8 | 5 | 37 |

| 19 | New York | 49.88 | 11 | 41 | 17 |

| 20 | Nevada | 47.06 | 7 | 8 | 48 |

| 21 | New Jersey | 46.85 | 19 | 44 | 13 |

| 22 | Tennessee | 46.48 | 17 | 6 | 39 |

| 23 | Wisconsin | 45.96 | 29 | 21 | 24 |

| 24 | Missouri | 45.95 | 30 | 25 | 16 |

| 25 | Delaware | 45.94 | 30 | 25 | 16 |

| 26 | Pennsylvania | 44.92 | 21 | 38 | 19 |

| 27 | Connecticut | 42.66 | 42 | 49 | 6 |

| 28 | Indiana | 42.58 | 31 | 24 | 30 |

| 29 | Iowa | 42.41 | 37 | 14 | 27 |

| 30 | North Dakota | 42.01 | 26 | 27 | 34 |

| 31 | Kansas | 41.74 | 24 | 29 | 33 |

| 32 | Nebraska | 41.36 | 36 | 12 | 35 |

| 33 | Illinois | 39.06 | 23 | 48 | 29 |

| 34 | South Carolina | 39.02 | 32 | 23 | 41 |

| 35 | Alabama | 38.87 | 34 | 30 | 36 |

| 36 | Ohio | 38.84 | 25 | 43 | 32 |

| 37 | Vermont | 38.57 | 48 | 34 | 22 |

| 38 | Montana | 38.39 | 46 | 19 | 31 |

| 39 | Oklahoma | 35.97 | 35 | 33 | 42 |

| 40 | South Dakota | 35.78 | 47 | 9 | 44 |

| 41 | New Mexico | 35.41 | 41 | 51 | 23 |

| 42 | Maine | 34.42 | 38 | 36 | 43 |

| 43 | Rhode Island | 33.52 | 50 | 39 | 28 |

| 44 | Wyoming | 32.52 | 45 | 40 | 40 |

| 45 | Kentucky | 31.74 | 33 | 45 | 46 |

| 46 | Arkansas | 30.17 | 43 | 32 | 50 |

| 47 | West Virginia | 28.92 | 40 | 42 | 51 |

| 48 | Hawaii | 28.80 | 51 | 28 | 47 |

| 49 | Mississippi | 28.63 | 44 | 46 | 45 |

| 50 | Louisiana | 28.53 | 39 | 47 | 49 |

| 51 | Alaska | 28.49 | 49 | 50 | 38 |

Not all economic growth strategies are effective. For the best ways to stimulate the economy and achieve lasting prosperity, we asked a panel of experts to share their thoughts on the following key questions:

John L. Campbell

John L. Campbell

Ph.D. – Professor, Department of Sociology, Dartmouth College

There is no one “most effective” way to do this. For example, Massachusetts offers a highly educated labor force. New Hampshire offers low tax rates. Other states, often in the south, offer low wages given their adoption of “right to work” legislation making it hard for unions to organize effectively.

It’s hard to say. One thing would be to fund education and encourage universities and technical schools to work with business to create effective training and re-skilling programs to keep workers’ skills up to date. A more aggressive approach is that of Vermont, which is now offering financial incentives for people to move into the state for work.

Sometimes there is evidence of a race to the bottom when, for example, states are competing for an automobile plant and try to out do each other by offering low taxes or limited term tax holidays where the firm pays no taxes for some period of time. You see the same thing sometimes when cities are competing for a professional sports franchise.

But remember that tax rates are not the only thing firms consider when making decisions about where to go or entrepreneurs are making decisions about where to start a company. Other things include, for instance:

..............................................................................................................................................................

Arthur I. Cyr

Arthur I. Cyr

Director, Clausen Center, Clausen Distinguished Professor, Carthage College

State and local government officials, and for that matter others, should do disciplined in depth research on the comparative advantages – and disadvantages of their economy, society, and government as well as other institutions.

Every state has distinctive characteristics and strengths. Part of the genius of the Founding Fathers was to recognize this in creating our federal system.

State and other governments should analyze distinctive strengths as well as challenges in retaining as well as attracting workers. This applies across the board occupationally, not just to “skilled workers”, and in terms of generations.

Wisconsin overall is an example of a state with sustained success in attracting business. The long term migration from Illinois is dramatic proof that an environment with relatively low taxes, no debt and a genuinely welcoming approach can succeed.

Infrastructure and related understanding of the importance of transportation also provides crucial advantage. Governor Mike Pence of Indiana, for example, led comprehensive planning for improved quality and better integration of transportation resources across the board. Neither Indiana nor Wisconsin has experienced a “race to the bottom.”

Entrepreneurs by definition are idiosyncratic and independent. Sensible investment incentives by government are useful, but an open, diverse and law abiding environment are important. American culture and history, not government, foster entrepreneurship.

Americans, or at least some Americans, are obsessed with finding insight through data. Basic indicators such as education, unemployment and crime are important. Beyond that, human insight and talent are key, and not easily quantified. Each state is different.

...................................................................................................................................................................

Nathan Jensen

Nathan Jensen

Ph.D. – Professor in the Department of Government, McCombs School of Business at The University of Texas - Austin

This is a difficult question and I am afraid that there isn’t a simple answer. Communities all have different problems as well as assets so there is no one size fits all policy. But one simple idea is that the first principal should be similar to doctors. Do no harm.

Many of the problems, economic or non-economic, for communities require considerable resources. These communities should be very careful with the tax base and expenditures so as not to divert resources away from schools, roads, or public goods.

This is another good question. First, it does require jobs in the area. A few states such as Vermont and Oklahoma have programs to attract teleworkers (those with jobs out of state) but these programs are rare. You need employers.

Second, it really does require a place that people want to live. This can mean the coasts, but many coastal cities have become so expensive that there are a number of affordable cities that attract the best and brightest. The research triangle in North Corolina and Austin, TX (where I live) are good examples.

Related to the last question, one huge advantage is a university or college in the area. This attracts human capital, and many of these graduates may choose to stay. But it also generates a lot of the amenities that makes a place desirable to live.

States often compete for business investment by offering tax breaks and other incentives.

The academic literature is very critical of these incentives. A recent piece by Tim Bartik at the Upjohn Institute finds that between 75%-98% of incentives goes to companies that were coming anyway. Another study notes that these incentives harm the fiscal health of communities.

These are many of the same factors that make a city attractive to anyone. But, an existing startup ecosystem, complete with incubators and accerators can be really helpful.

![]()