When most people think of credit card perks their minds turn to rewards, low interest rates and the like. However, credit cards naturally provide a number of far reaching standard benefits that help protect cardholders from both monetary loss and unnecessary hassle. One of these benefits is car rental collision protection which is primarily driven by the card network and not the card issuer.

To provide context, roughly 20% of consumers always purchase supplemental insurance coverage when renting a car, according to a study from Progressive Insurance, and another 20% do so on occasion. Sitting atop the list of reasons for such purchases is confusion as to whether personal auto insurance extends to rental cars.

Indeed, 62% of consumers do not believe their personal auto insurance automatically covers rental cars, according to a survey conducted by the National Association of Insurance Commissioners. Similarly, 24% aren't sure whether their credit cards provide any sort of coverage either.

In this report, CardHub provides an in depth examination of each major card network's rental car insurance policy and explains what type of rental car insurance coverage consumers automatically receive through their credit cards, how they can take advantage of it, which credit cards offer the best insurance coverage, and whether any other forms of supplemental insurance are needed.

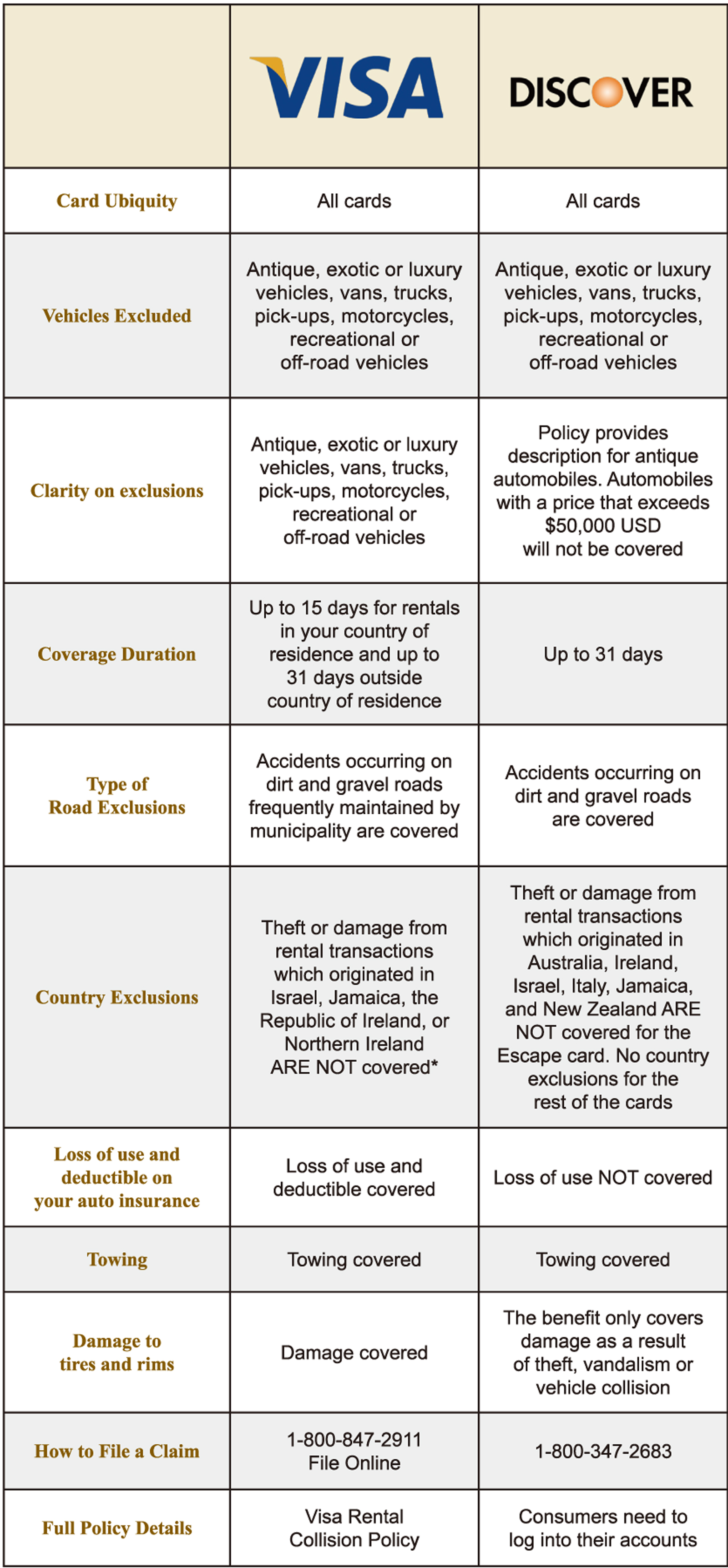

All four major card networks provide some form of rental car insurance coverage.

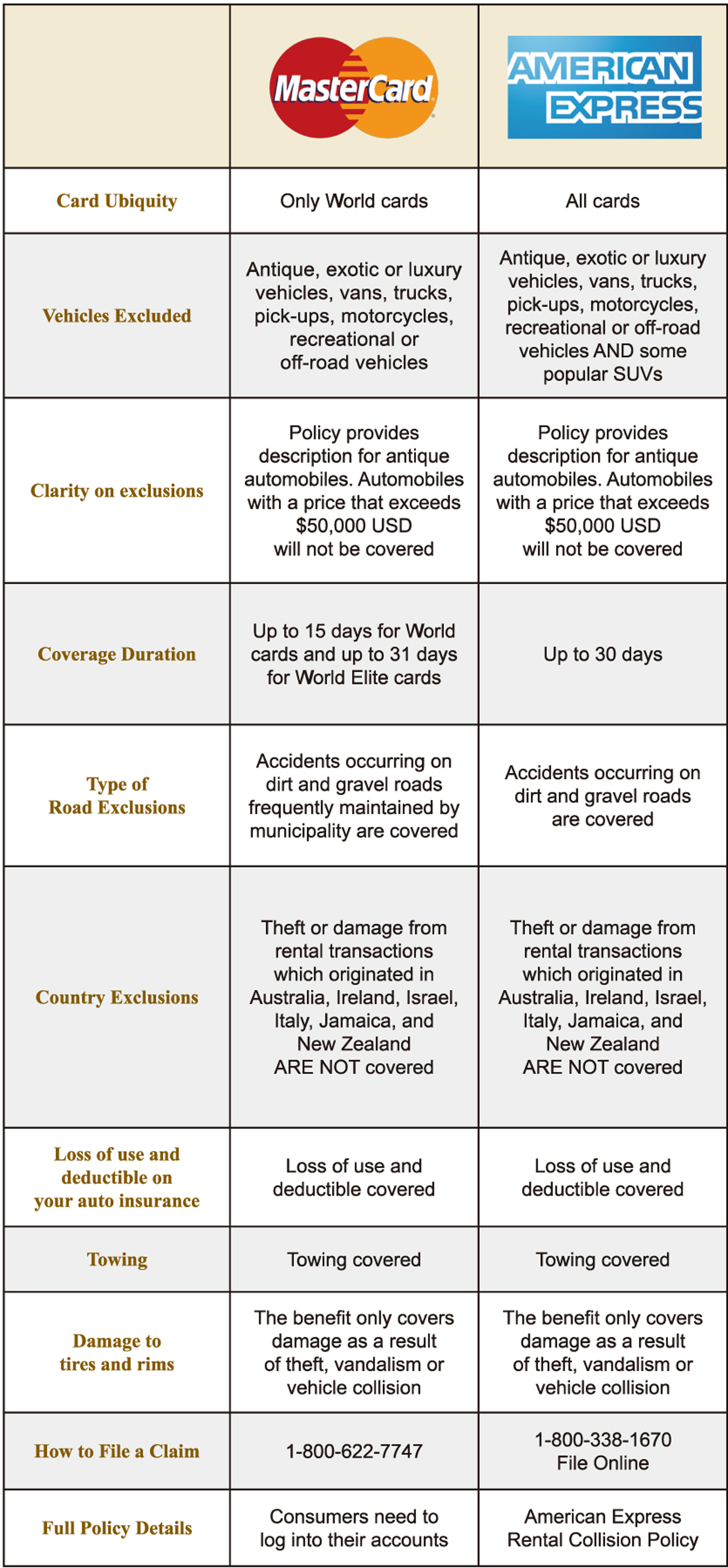

MasterCard is the only network that does not provide coverage on all of its cards.

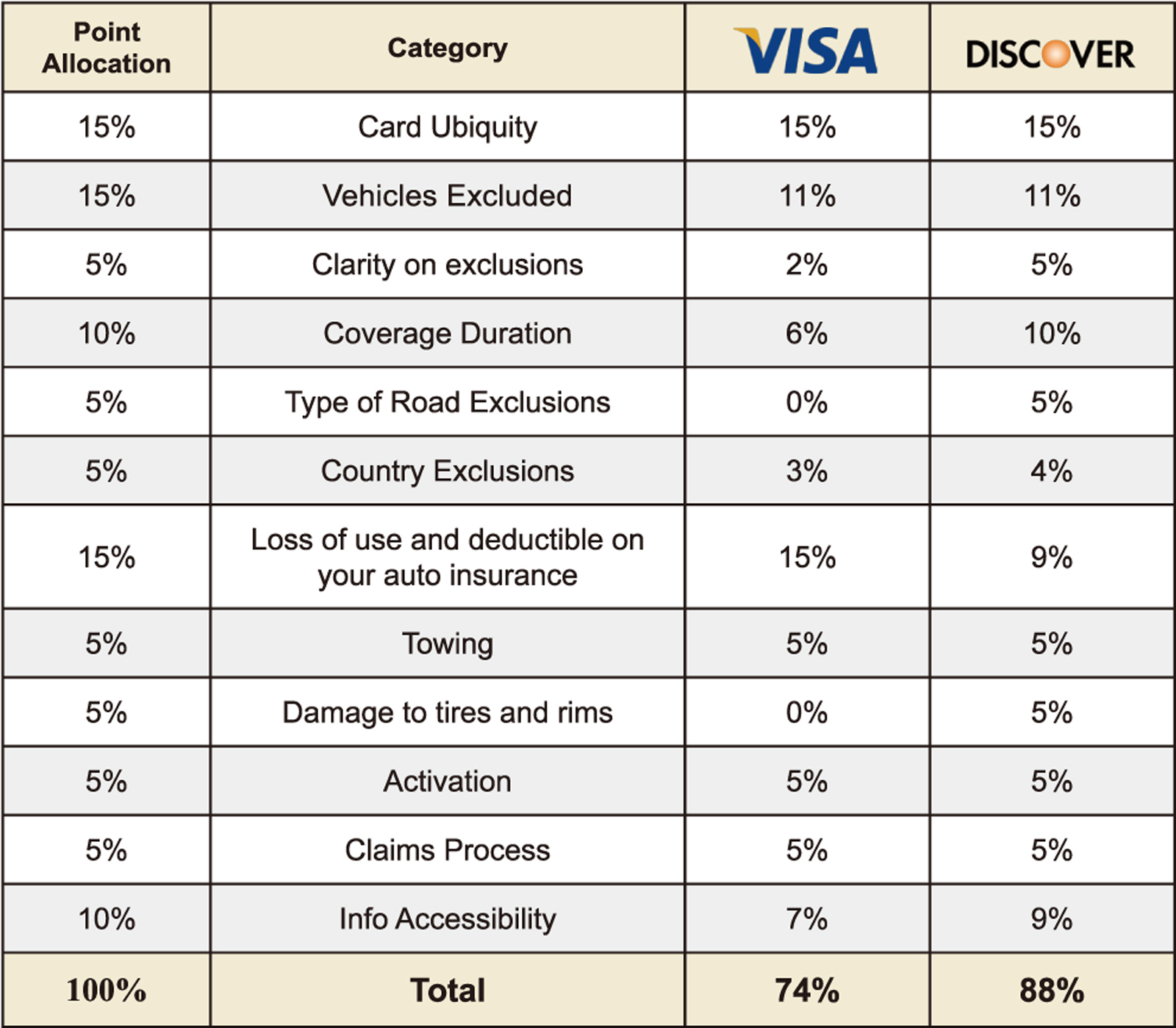

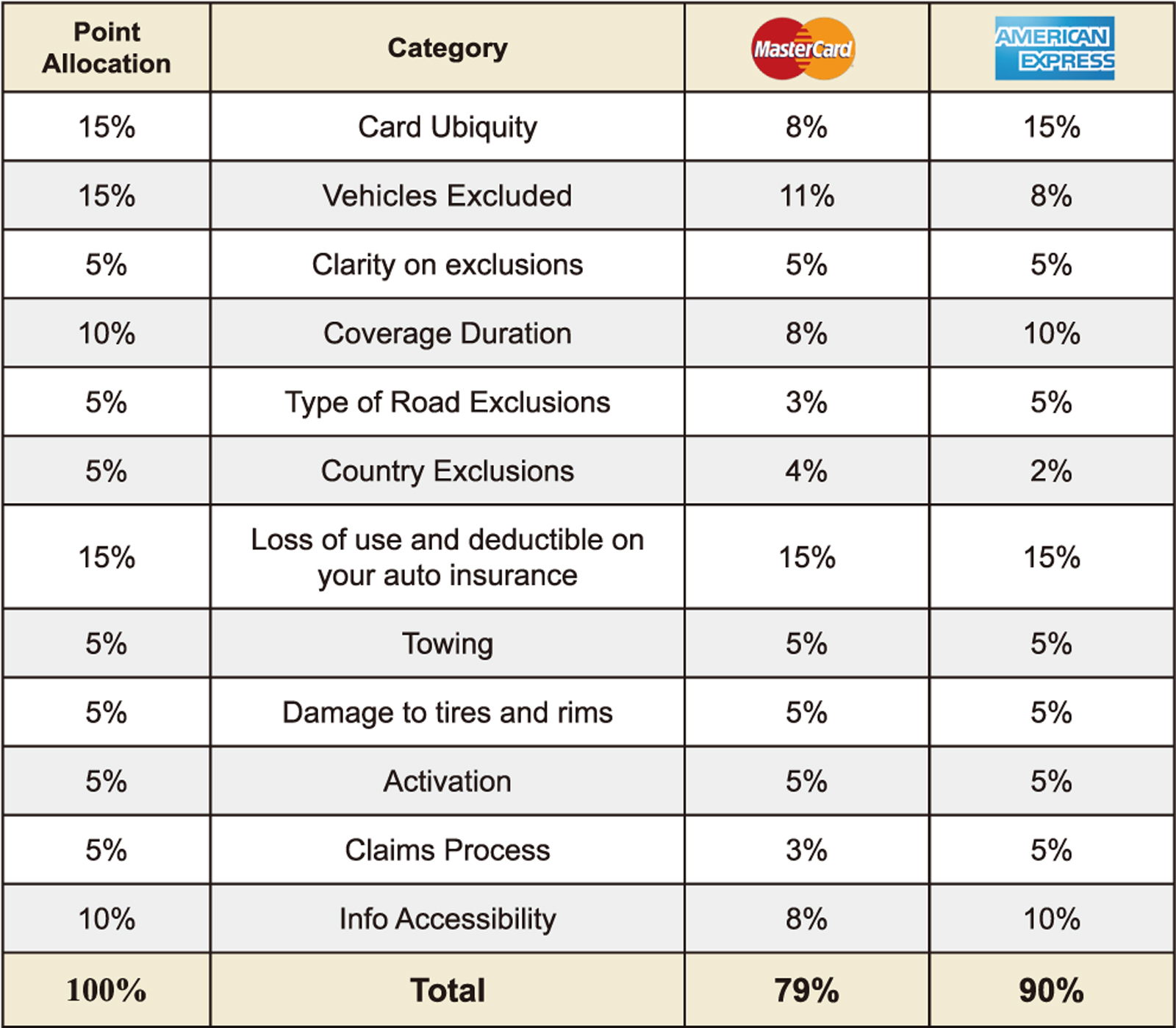

American Express received the highest cumulative score (90%) for its rental car insurance policy, while Visa ranked second (88%), Discover ranked third (79%) and Mastercard ranked last (74%).

All four major networks require cardholders to charge their entire rental car purchase on their credit card and decline supplemental insurance/Collision Damage Waivers (CDW) offered by the rental company in order to be eligible.

None of the four major networks provides coverage for the rental of: 1) exotic, expensive, or antique cars; 2) trucks; 3) vehicles with open beds; or 4) off-road vehicles.

VISA is the only network that does not cover accidents occurring on dirt and gravel roads. MasterCard only covers accidents on dirt and gravel roads if they are "regularly maintained."

All card networks exclude rentals that exceed specified time limits, and a lot of cards come with country limitations as well.

American Express is the only network not to provide coverage for renting certain popular SUVs — including the Suburban and Tahoe from Chevrolet, GMC Yukon, Ford Expedition, Lincoln Navigator, Toyota Land Cruiser, Lexus LX450, Range Rover, and full sized Ford Bronco.

All networks also provide roadside assistance to their cardholders for a pre-negotiated fee.

We have listed the basic coverage offered by Visa, however, some cards do not have the above listed country exclusions.

In the "Vehicles Excluded" category, we subtracted 4% because there are some exclusions attached to the benefit even though they are standard across all credit networks.

Under "Clarity on Exclusions," we subtracted 3% because the maximum value of cars that are eligible for the benefit is not disclosed.

In the "Coverage Duration" category, the network received 6% because the length of coverage is limited to 15 days.

Under "Type of Road Exclusions," we did not award any points because accidents occurring on dirt or gravel roads are not covered under the benefit.

For "Country Exclusions," a 2% penalty was applied because four countries are excluded from coverage.

In the "Damage to Tires and Rims" category, no points were awarded as the benefit does not apply to this type of damage.

Under "Info Accessibility," Visa scored 7% because their policy disclosure is in small print and they refused to participate when contacted for clarifications.

In the "Vehicles Excluded" category, we subtracted 4% because there are some exclusions attached to the benefit even though they are standard across all credit networks.

For "Country Exclusions," a 1% penalty was assessed because the Escape cards exclude six countries from coverage.

In the "Loss of Use and Deductible on Your Auto Insurance" category, the network received 9% because its policy does not cover loss of use for rental cars.

Under "Info Accessibility," Discover scored 9% because consumers need to log in to access the disclosure.

Under "Card Ubiquity," we have subtracted 7% because the network does not provide information about the type of coverage provided for all of their cards.

Under the "Vehicles Excluded" category, we subtracted 4% because there are some exclusions attached to the benefit even though they are standard across all credit networks.

In the "Coverage Duration" category, we awarded 8% points — the average obtained from scoring the network's two policies; 10% for coverage over 31 days and 6% for coverage of19-10 days.

Under "Type of Road Exclusions," we awarded only 3% points because accidents occurring on dirt or gravel roads are only covered if the road is frequently maintained by the municipality.

For "Country Exclusions," a 4% score was applied — the average for both of the network's policies; 5% points for no country exclusions and 3% points for four countries excluded from coverage.

Under "Claims Process," we awarded only 3% because this process requires more documents in order for a claim to be validated.

MasterCard received an "Info Accessibility" score of 8% because the disclosure is in small print and consumers need to log in to access it.

Under the "Vehicles Excluded" category, we subtracted 7% because there are some exclusions attached to the benefit even though they are standard across all credit networks, and given that the benefit does not cover some popular SUV's.

For "Country Exclusions," a 3% penalty was applied because six countries are excluded from coverage.

Call your insurance company and find out if rentals are covered under your standard policy. Older policies may not offer this coverage.

Call your credit card issuer and ask what limitations apply to the car rental coverage provided by your particular type of credit card.

It might be wise to accept the liability insurance and collision damage waiver offered by the car rental company if you do not have personal auto insurance and your credit card does not provide sufficient coverage.

Long term rentals might not be covered by your existing auto insurance as time limitations may be imposed by your policy.

Your personal auto policy, if it even covers rentals, only applies when the vehicle is used for personal use. So, if you're traveling for business, check what other options are available for you.

Rent a car of similar value to your own car in order to increase the likelihood that your existing coverage is also adequate for the rental car.

Sometimes, when your existing policy does not offer coverage for a particular type of rental car, you can ask about the possibility of adding an insurance rider for a small fee.

If you are not a car owner but drive from time to time, you might want to consider purchasing a non-owner auto insurance policy.