Aug 29, 2018

John S Kiernan, Senior Writer & Editor

Consumer research and ratings firm J.D. Power has released its July auto sales forecast, and the trends aren't looking great for the industry. Monthly new vehicle retail sales had increased for the previous 54 months compared to the same months in the previous year.

However, July's sales were projected to have a 3.2% decrease compared to July 2017. But with dealers having offered even bigger savings during Labor Day weekend, especially on older models, potential buyers will certainly be asking if now is a good time to purchase a car.

At the moment, the market appears to be tilting in favor of the consumer. But there are more questions than just whether or not to buy. Should buyers apply for financing from banks, credit unions or manufacturers? Which manufacturers offer the best financing and leasing terms? How do interest rates compare for new versus used vehicles?

WalletHub answers these questions and more below, based on a detailed analysis of financing offers from a diverse group of more than 150 lenders. The data provided in this report, along with the panel discussion featuring industry experts, will help you make an informed decision.

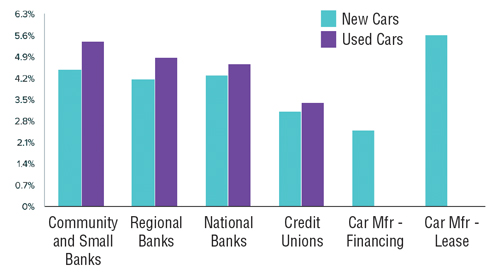

Interest Rates for New & Used Cars

Financing Offers by Car Manufacturer

It is important for consumers to understand that car-dealership financing offers may come from the financing arm of a car manufacturer or from a third-party financial institution. The following offers reflect financing available directly from car manufacturers' financing arms.

Car Manufacturer |

Financing APR Q3 2018 |

Lease APR (inferred interest rate) Q3 2018 |

Honda |

1.90% |

7.31% |

Toyota |

1.90% |

2.95% |

Volkswagen |

1.90% |

4.57% |

Chevrolet |

7.49% |

6.49% |

BMW |

5.59% |

5.25% |

Nissan |

4.00% |

5.25% |

Hyundai |

3.99% |

7.21% |

Kia |

0.00% |

7.93% |

Mazda |

0.00% |

5.88% |

Acura |

1.90% |

4.57% |

Ford |

0.00% |

4.33% |

Audi |

4.99% |

5.34% |

Infiniti |

0.00% |

3.00% |

Subaru |

0.00% |

2.79% |

Lexus |

2.99% |

5.38% |

Mercedes |

3.99% |

5.01% |

Dodge |

0.00% |

6.05% |

Volvo |

3.59% |

6.83% |

Mini |

1.90% |

7.81% |

Buick |

4.00% |

8.39% |

Average |

2.51% |

5.62% |

Note: Above data are based on a 36-month term. The APRs presented for the financing and lease programs of the car manufactures are informational only. The actual obtainable values are based on various factors, including the borrower's creditworthiness, income, location of residence, promotional programs and even negotiation skills.

Make sure to always check upfront with a dealer about the availability of any discounts for particular groups (e.g., military personnel with USAA membership) that you might qualify for and any other costs/restrictions that may be imposed, especially in the case of lease contracts.

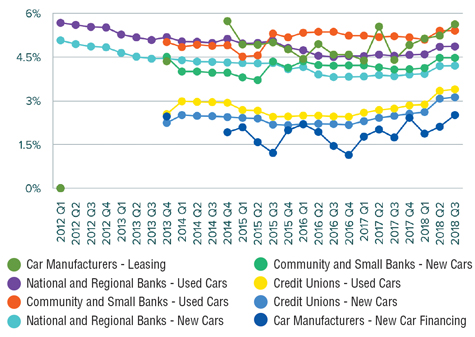

Historical Interest Rates

Note: Above data is based on a 36-month term.

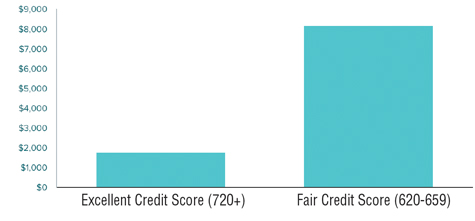

Excellent vs. Fair Credit Score - Interest Paid over a 5 Year Car Loan

Note: Above data reflects a $20,000 five-year loan for a new car with a fixed interest rate, using WalletHub's interest-rate data from Q3 2018.

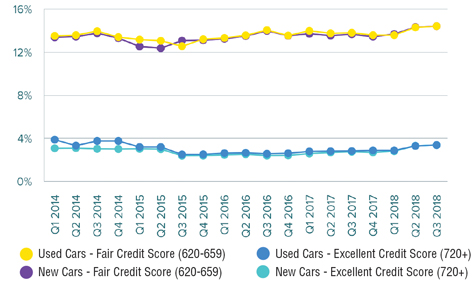

Excellent vs. Fair Credit Score Over Time

Manufacturer Transparency Based on Maximum of 10

Maufacturer |

Transp. Score - Q3 2018 |

Mini |

6 |

BMW |

6 |

Mercedes |

6 |

Honda |

6 |

Toyota |

6 |

Nissan |

6 |

Audi |

6 |

Hyundai |

6 |

Mazda |

5 |

Acura |

5 |

Subaru |

5 |

Infiniti |

3 |

Volkswagen |

3 |

Kia |

3 |

Ford |

3 |

Dodge |

3 |

Lexus |

3 |

Buick |

3 |

Cadillac |

3 |

Chevrolet |

3 |

Chrysler |

3 |

Volvo |

2 |

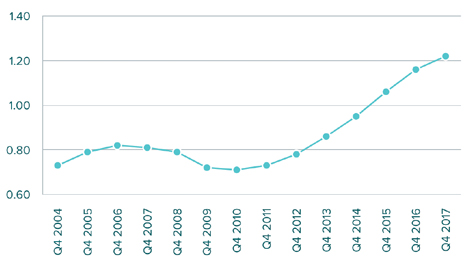

Total Auto-Debt Balance over Time ($ Trillion)

Source: Federal Reserve Bank of New York

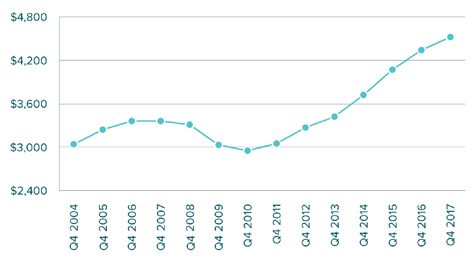

Per-Capita Auto-Debt Balance over Time

Source: Federal Reserve Bank of New York

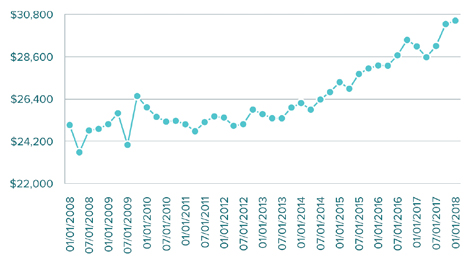

Average Amount Financed for New Car Loans at Finance Companies (Quarterly)

Source: Federal Reserve Bank of St. Louis

Average Amount Financed for Used Car Loans at Finance Companies (Quarterly)

Source: Federal Reserve Bank of St. Louis

If you aren't carefully monitoring the trends in car sales, you might miss out on a good deal — or buy at the wrong time. For additional insight into the car buying process and related issues, we asked a panel of experts to weigh in with their thoughts on the following key questions:

|

Contributing Writer for Jalopnik |

On a scale of 1 (an emphatic no) to 10 (an emphatic yes), is this a good time of year to buy a car?

I would say an 8 or a 9, the best time to buy a car is when you are ready not just when there are a bunch of advertised deals. Now is a good time to get a deal on a leftover model, but act fast because if you wait until all the 2019 models are on the ground the available inventory on 2018 models may be too slim.

Do you expect auto financing deals to improve/get worse/stay the same over the next 12 months?

Despite the Fed increasing rates, financing has stayed pretty competitive. It's hard to predict what will happen. I don't think it's going to get any better than some of the low APR specials that some of the manufacturers are running. If anything it will either remain status quo or the rates will start to creep up.

What steps can buyers and dealers take to make the car buying process more transparent and hassle-free?

Buyers should do their research and do not negotiate in person. Request written quotes via email and compare before walking into the dealership. If a dealer doesn't want to provide this time of buying process, give someone else the business.

What tips do you have for individuals with fair or poor credit who are looking for an auto loan?

If your credit isn't great it is imperative that you get pre-approved for a car loan through a credit union, local bank or other financial institution. There are even online lenders that can help. This pre-approval will give you leverage against a dealer that comes back with a high APR loan and turns you into a cash buyer. In this way you don't have to worry about a dealer trying to win back the deal after the fact because financing fell through.

What are some signs that you may be getting ripped off in the auto financing process?

Buyers need to do the math before they sign the papers. Take the monthly payments and multiply it by the loan term, then look at the total. If that total amount is dramatically more expensive than the price of the car you are buying, chances are that's a bad deal. Here is an example, I had a client that was looking for a minivan with an advertised price of about $18,000, the dealer quoted them payments of $365/month for 72 months, that's $26,280 and these folks had good credit. The dealer was both marking up the rate and packing in all kinds of add-ons and extra fees.

|

Dealer Principal |

On a scale of 1 (an emphatic no) to 10 (an emphatic yes), is this a good time of year to buy a car?

10 for new cars based on factory incentives, dealers' desire to clear out 2018 models and strong used vehicle prices (trade-in is worth all the money); 5 for used vehicles based on strong used vehicle prices and higher interest rates.

Do you expect auto financing deals to improve/get worse/stay the same over the next 12 months?

Definitely get worse, we anticipate interest rates to rise over the next 12 months.

What steps can buyers and dealers take to make the car buying process more transparent and hassle free?

Buyers should do their research before coming to a dealership. Try to find a dealer or salesperson they trust. If they don't know any, ask a friend or co-worker who has recently bought a vehicle. Then go into the store. A dealer cannot give a fair appraisal unless they see your vehicle. It is important for buyers to be honest as well as dealers. Be open and honest about trade, payoff, expectations, etc. Demand that same honest from dealership.

What tips do you have for individuals with fair or poor credit who are looking for an auto loan?

We can almost always get someone financed. It may take more down payment or a co-buyer. So if you don't have a co-buyer or enough down, wait until you do. It is important for someone with less than prime credit to understand how important it is to consider a vehicle that will help them get back on track. That may mean one with a few more miles on it, better fuel economy, not the perfect color, etc. Drive this vehicle for 18-24 months until you can get your credit back to where you are a prime buyer.

What are some signs that you may be getting ripped off in the auto financing process?

It is important to understand all the terms in your contract – rate, term and amount financed. The finance manager should review these terms with the buyer.

|

Owner & Founder, |

My advice is almost always to buy a gently used vehicle, pay as much as you can in cash,

and to finance as little as possible or not at all. Following that plan, auto financing deals are irrelevant. Cars are the most expensive thing we buy that goes down in value, and they do so the fastest of all.

Behaviourally speaking we're willing to finance a more expensive car than we'd otherwise pay for in cash because we focus on the affordability of the monthly payment rather than the purchase price.

We pay a premium when we buy a brand new car which can easily lose 15% - 20% of its value in the first year alone, and another 10% or so each year after that. Flashy marketing and financing deals lure car buyers into paying a premium price on new vehicles.